A number of days in the past, I valued Instacart forward of its preliminary public providing, and famous that the reception that the inventory will get can be a superb barometer of the place danger capital stands out there, proper now. After a buzzy open, when the inventory jumped from its providing value of $30 a share to $42, the inventory has shortly given up these good points and now trades at beneath to its supply value. On this put up, I’ll have a look at one other preliminary public providing, Birkenstock, that’s more likely to get extra consideration within the subsequent few weeks, provided that it’s focusing on to go public at a pricing of about €8 billion, for its fairness, in just a few weeks. Moderately than make this put up all about valuing Birkenstock, and evaluating that worth to the proposed pricing, I want to use the corporate to debate how intangible belongings get valued in an intrinsic valuation, and why a lot of the dialogue of intangible valuation in accounting circles is a mirrored image of a mind-set on valuation that always misses its essence.

The Worth of Intangible Property

Accounting has traditionally carried out a poor job coping with intangible belongings, and because the economic system has transitioned away from a manufacturing-dominated twentieth century to the know-how and providers targeted economic system of the twenty first century, that failure has develop into extra obvious. The ensuing debate amongst accountants about easy methods to deliver intangibles on to the books has spilled over into valuation observe, and lots of appraisers and analysts are wrongly, in my opinion, letting the accounting debate have an effect on how they worth firms.

The Rise of Intangibles

Whereas the talk about intangibles, and the way greatest to worth them, is comparatively current, it’s unquestionable that intangibles have been part of valuation, and the funding course of, by way of historical past. An analyst valuing Common Motors within the Nineteen Twenties was in all probability attaching a premium to the corporate, as a result of it was headed by Alfred Sloan, seen then a visionary chief, simply as an investor pricing GE within the Nineteen Eighties was arguing for a better pricing, as a result of Jack Welch was engineering a rebirth of the corporate. Even a cursory examination of the the Nifty Fifty, the shares that drove US equities upwards within the early Nineteen Seventies, reveals firms like Coca Cola and Gilette, the place model title was a major contributor to worth, in addition to pharmaceutical firms like Bristol-Myers and Pfizer, which derived a big portion of their worth from patents. In actual fact, IBM and Hewlett Packard, pioneers of the tech sector, have been priced increased throughout that interval, due to their technological strengths and different intangibles. Inside the funding neighborhood, there has all the time been a transparent recognition of the significance of intangibles in driving funding worth. In actual fact, amongst old-time worth traders, particularly within the Warren Buffet camp, the significance of getting “good administration’ and moats (aggressive benefits, lots of that are intangible) represented an acceptance of to how important it’s that we incorporate these intangible advantages into funding selections.

With that mentioned, it’s clear that the talk about intangibles has develop into extra intense within the final 20 years. One motive is the notion that intangibles now symbolize a higher p.c of worth at firms and are a major issue in additional of the businesses that we spend money on, than previously. Whereas I’ve seen claims that intangibles now account for sixty, seventy and even ninety p.c of worth, I take these contentions with a grain of salt, because the definition of “intangible” is elastic, and a few stretch it to breaking level, and the measures of worth used are questionable. A extra tangible solution to see why intangibles have develop into a sizzling matter of debate is to have a look at the evolution of the highest ten firms on the earth, in market capitalization, over time:

In 1980, IBM was the biggest market cap firm on the earth, however eight of the highest ten firms have been oil or manufacturing firms. With every decade, you may see the impact of regional and sector efficiency within the earlier decade; the 1990 record is dominated by Japanese shares, reflecting the rise of Japanese equities within the Nineteen Eighties, and the 2000 record by know-how and communication firms, benefiting from the dot-com growth. Wanting on the prime ten firms in 2020 and 2023, you see the dominance of know-how firms, lots of which promote merchandise that you simply can not see, usually in manufacturing services which can be simply as invisible.

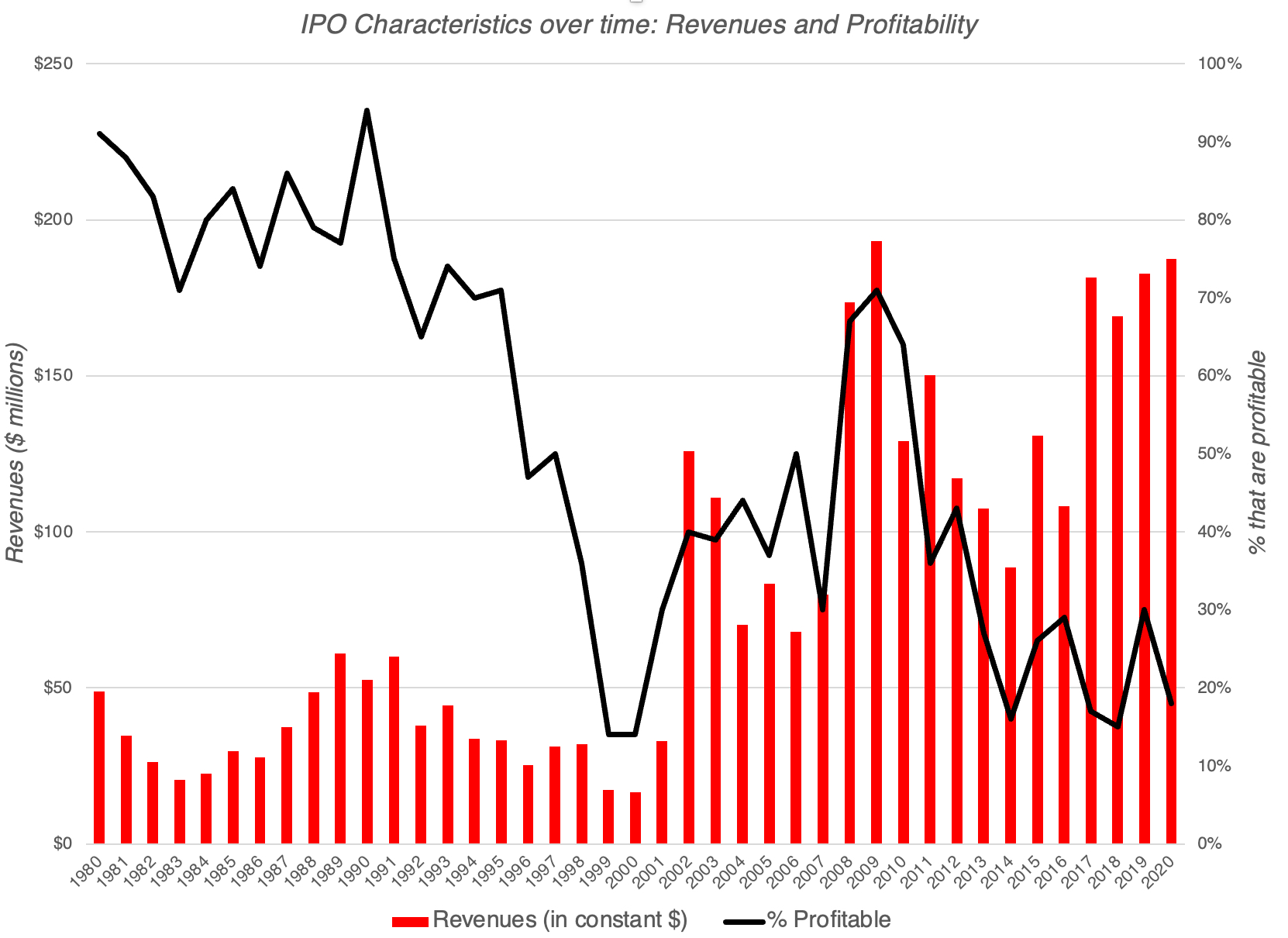

The opposite growth that has pushed the intangible dialogue to the forefront is a sea change within the traits of firms coming into public markets. Whereas firms that have been listed for a lot of the 20th century waited till they’d established enterprise fashions to go public, the dot-com growth noticed the itemizing of younger firms with development potential however unformed enterprise fashions (translating into working losses), and that pattern has continued and accelerated on this century. The graph beneath appears to be like on the revenues and profitability of firms that go public every year, from 1980 to 2020:

As you may see, the p.c of money-making firms going public has dropped from greater than 90% within the Nineteen Eighties to lower than 20% in 2020, however on the identical time, whereas additionally reporting a lot increased revenues, reporting the push by personal firms to scale up shortly. In valuing these firms, traders and analysts face a problem, insofar as a lot of the values of those corporations got here from expectations of what they’d do sooner or later, fairly than investments that they’ve already made. I seize this impact in what I name a monetary stability sheet:

When you can worth assets-in-place, utilizing historic knowledge and the knowledge in monetary statements, in assessing the worth of development belongings, you’re making your greatest assessments of investments that these firms will make sooner or later, and these investments are formless, a minimum of for the time being.

The Accounting Problem with Intangibles

The intangible debate is most intense within the accounting neighborhood, with each practitioners and teachers arguing about whether or not intangibles ought to be “valued”, and in that case, easy methods to deliver that worth into monetary statements. To see why the accounting penalties are more likely to be dramatic, contemplate how these decisions will play out within the stability sheet, the accountants’ try to encapsulate what a enterprise owns, what it owes and the way a lot its fairness is value.

There are inconsistencies in how accountants measure totally different lessons of belongings, and I incorporate them into my image above, leaving the intangible belongings part because the unknown: Any modifications in accounting guidelines on measuring the worth of intangibles, and bringing them on the stability sheet, will even play out as modifications on the opposite facet of the stability sheet, primarily as modifications within the worth of assessed or guide fairness. Put merely, if accountants resolve to deliver intangible belongings like model title, administration high quality and patent safety into asset worth will improve the worth of guide fairness, a minimum of as accountants measure it, in that firm.

Of their try to deliver intangible belongings on to stability sheets, accountants face a barrier of their very own creation, emanating from how they deal with the expenditures incurred in build up these belongings. To grasp why, contemplate how fastened belongings (comparable to plant and gear and gear) develop into a part of the stability sheet. The expenditures related to buying these fastened belongings are handled as capital expenditures, separate from working bills, and solely the portion of that expenditure (depreciation or amortization) that’s assumed to be associated to the present 12 months’s operations is handled as an working expense. The unamortized or un-depreciated parts of those capital bills are what we see as belongings on stability sheets. The bills that lead to intangible asset acquisitions are, for probably the most half, not handled persistently, with model title promoting, R&D bills and investments in recruiting/coaching, the bills related to build up model title, patent safety and human capital, respectively, being handled as working, fairly than capital, bills. As a consequence of this mistreatment, I’ve argued that not solely are the most important belongings, largely intangible, at some firms saved off the stability sheet, however their earnings are misstated:

There are methods by which accounting can repair this inconsistency, however it can lead to an overhaul of the entire monetary statements, and firms and traders balk at wholesale revamping of accounting numbers (EBITDA, earnings per share, guide worth) that they’ve relied on to cost these corporations.

So, how far has accounting are available in bringing intangible belongings on to stability sheets? One solution to measure progress on this concern is to have a look at the portion of the guide worth of fairness at US firms that comes from tangible belongings, within the chart beneath:

Wanting throughout all US corporations from 1980 to 2022, the portion of guide worth of fairness that comes tangible belongings has dropped from greater than 70% in 1998 to about 30% in 2022. That will recommend that intangible belongings are being valued and integrated into stability sheets rather more now than previously. Earlier than you come to that conclusion, although, you could need to contemplate the breakdown of the intangible belongings on accounting stability sheets, which I do within the graph beneath:

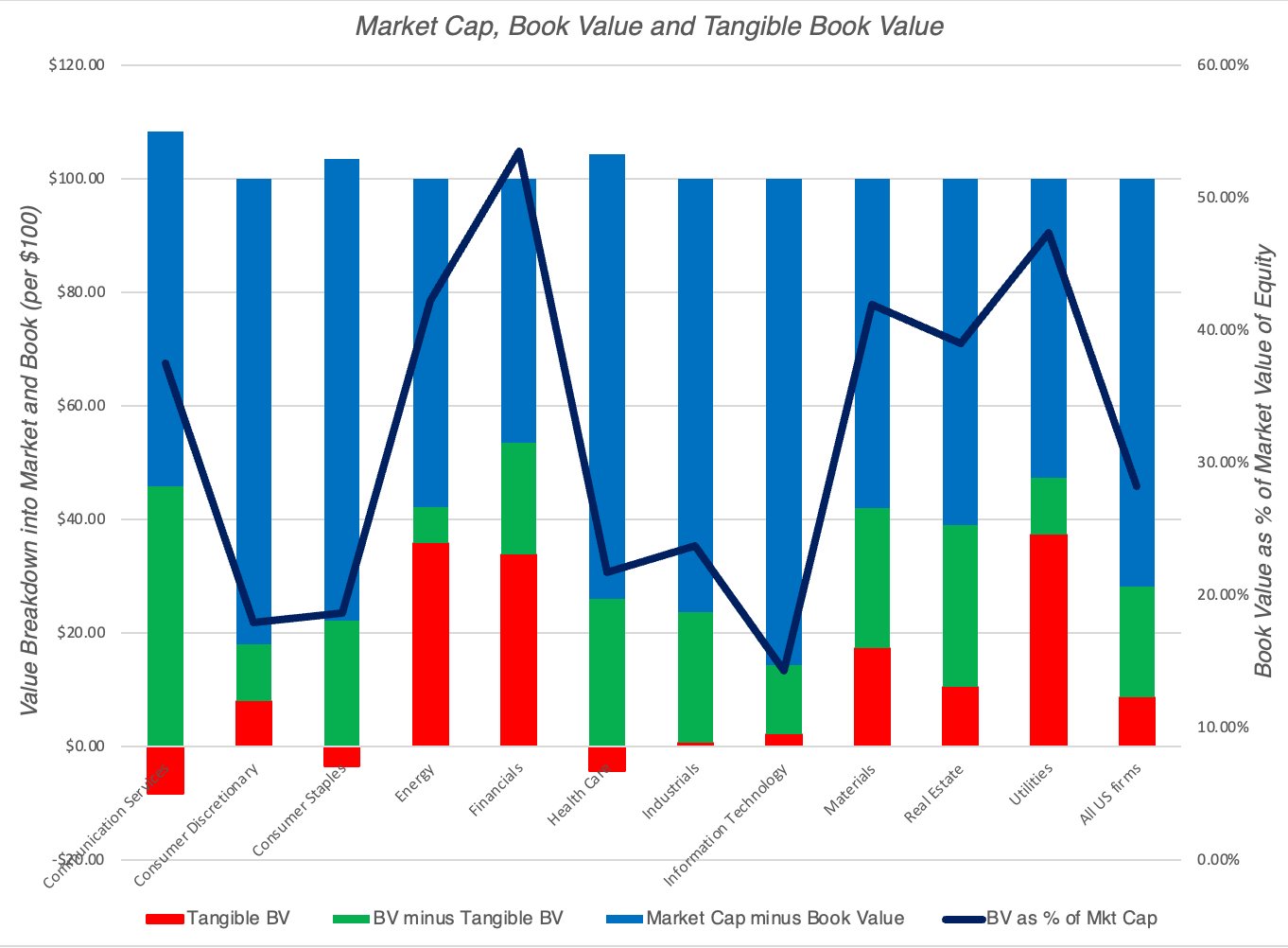

There may be one other measure that you need to use to see the futility, a minimum of up to now, of accounting makes an attempt to worth intangibles. Within the graph beneath, I have a look at the aggregated market capitalization of firms, in 2022, which ought to incorporate the pricing of intangibles by the market, and examine that worth to guide worth (tangible and intangible), by sector, reflecting accounting makes an attempt to worth these identical intangibles.

The sectors the place you’ll anticipate intangible belongings to be the biggest portion of worth are client merchandise (model title) and know-how (R&D and patents). These are additionally the sectors with the bottom guide values, relative to market worth, suggesting that no matter accountants are doing to usher in intangibles in these firms into guide worth just isn’t having a tangible impact on the numbers.

In sum, the accounting obsession with intangibles, and the way greatest to take care of them, has not translated into materials modifications on stability sheets, a minimum of with GAAP in the US. It’s true that IFRS has moved quicker in bringing intangible belongings on to stability sheets, albeit not all the time in probably the most smart methods, however even with these guidelines in place, progress on bringing intangible belongings onto stability sheets has been gradual. To be frank, I do not assume accounting rule writers will be capable to deal with intangibles in a smart method, and the boundaries lie not in guidelines or fashions, however within the accounting mindset. Accounting is backward-looking and rule-driven, making it sick geared up to worth intangibles, the place you haven’t any selection, however to be ahead wanting, and principle-driven.

The Intrinsic Worth of Intangibles

I’ve been educating and writing about valuation for near 4 many years now, and I’ve usually been accused of giving quick shrift to intangible belongings, as a result of I haven’t got a session devoted to valuing intangibles, in my valuation class, and I haven’t got complete books, and even chapters of my books, on the subject. Whereas it could appear to be I’m in denial, given how a lot worth firms derive from belongings you can not see, I’ve by no means felt the necessity to create new fashions, and even modify current fashions, to usher in intangibles. On this part, I’ll clarify why and make the argument that when you do intrinsic valuation proper, intangibles ought to be, with creativeness and little or no modification of current fashions, already in your intrinsic worth.

To grasp intrinsic worth, it’s value beginning with the easy equation that animates the estimation of worth, for an asset with n years of money flows:

Thus, the intrinsic worth of an asset is the current worth of the anticipated money flows on it, over its lifetime. When valuing a enterprise, the place money flows might final for for much longer (even perhaps eternally), this equation could be tailored:

On this equation, for something, tangible or not, has to indicate up in both the anticipated money flows or within the danger (and the ensuing low cost fee); that’s my “IT” proposition. This proposition has stood me in good stead, in assessing the impact on worth of nearly every little thing, from macro variables like inflation to buzzwords like ESG.

Utilizing this framework for assessing intangible belongings, from model title to high quality administration, you may see that their impact on worth has to return from both increased anticipated money flows or decrease danger (low cost charges). To offer extra construction to this dialogue, I reframe the worth equation when it comes to inputs that valuation analysts ought to be accustomed to – income development, working margins and reinvestment, driving money flows, and fairness and debt danger, figuring out low cost charges and failure danger.

Within the image, I’ve spotlight among the key intangibles and which inputs are largely more likely to be affected by their presence.

- It’s the working margin the place model title, and the related pricing energy, is probably going have its greatest impact, although it could possibly have secondary results on income development and even the price of capital.

- Good administration, one other extremely touted intangible, will manifest in a enterprise with the ability to ship increased income development, but in addition present up in margins and reinvestment; the essence of superior administration is with the ability to discover development, when it’s scarce, whereas sustaining profitability and never reinvesting an excessive amount of.

- Connections to governments and regulators, an intangible that’s seldom made specific, can have an effect on worth by decreasing failure danger and the price of debt, whereas rising development and or profitability, as the corporate will get favorable therapy on bids for contracts.

This isn’t a complete record, however the framework applies to any intangible that you simply consider might impact worth. This strategy to intangibles additionally means that you can separate helpful intangibles from wannabe intangibles, with the latter, irrespective of how broadly bought, having little or no impact on worth. Thus, an organization that claims that it has a helpful model title, whereas delivering working margins effectively beneath the trade common, actually doesn’t, and the impact of ESG on worth, it doesn’t matter what its advocates declare, is non-existent.

It’s true that this strategy to valuing intangibles works greatest for an organization with a single intangible, whether or not it’s model title or buyer loyalty, the place the impact is remoted to one of many worth drivers. It turns into harder to make use of for firms, like Apple, with a number of intangibles (model title, styling, working system, person platform). When you can nonetheless worth Apple within the combination, breaking out how a lot of that worth comes from every of the intangibles can be tough, however as an investor, why does it matter?

The Birkenstock IPO: A Footwear firm with intangibles

When you’ve got discovered this dialogue of intangibles summary, I do not blame you, and I’ll attempt to treatment that by making use of my intrinsic worth framework to worth Birkenstock, simply forward of its preliminary public providing. As a firm with a number of intangible elements in its story, it’s effectively suited to the train, and I’ll attempt to not solely estimate the worth of the corporate with the intangibles integrated into the numbers, but in addition break down the worth of every of its intangibles.

The Lead In

Birkenstock is primarily a footwear firm, and to get perspective on development, profitability and reinvestment within the sector, I checked out all publicly traded footwear firms throughout the globe. the desk beneath summarizes key valuation metrics for the 86 listed footwear firms that have been listed as of September 2023.

Within the combination, the metrics for footwear firms are indicative of an unattractive enterprise, with greater than half the listed firms seeing revenues shrink within the decade, main into 2022 and greater than quarter reporting working losses. Nonetheless, many of those firms are small firms, with a median income at $170 million, struggling to remain afloat in a aggressive product market. Since Birkenstock generated revenues of $1.4 billion within the twelve months main into its preliminary public providing, with an expectation of extra development sooner or later, I zeroed in on the twelve largest firms within the attire and footwear sector, in market capitalization, and checked out their working metrics:

As you may see, these firms look very totally different from the sector aggregates, with strong income development (median compounded development fee of 8.66% a 12 months, for the final decade) and distinctive working margins (gross margins near 70% and working margins of 24%). Every of the businesses additionally has a recognizable or many recognizable model names, with LVMH and Hermes topping the record. On this enterprise, a minimum of, model title appears to be dividing line between success and mediocrity, and having a well-recognized model title contributes to development and profitability. It’s this grouping that I’ll draw on extra, as I look valuing Birkenstock.

Birkenstock’s Historical past

In my work on company life cycles, I discuss how firms age, and the way significance it’s that they act accordingly. Typically, as an organization strikes throughout the life cycle, income development eases, margins stage off and there may be much less reinvestment. As a enterprise that has been round for nearly 250 years, Birkenstock ought to be a mature and even outdated firm, nevertheless it has discovered a brand new lease on life within the final decade.

Birkenstock was based in 1774 by Johann Adam Birkenstock, a Germany cobbler, and it stayed a household enterprise for a lot of its life. Within the many years following its founding, the corporate modified and tailored its footwear choices, catering to rich Europeans within the rising German spa tradition within the 1800s, and modifying its product line, including versatile insoles in 1896 and pioneering arch helps in 1902. Through the Nineteen Twenties and Nineteen Thirties, the corporate carved out a market round consolation and foot care, partnering with physicians and podiatrists, providing options for purchasers with foot ache. In 1963, the corporate launched its first health sandal, the Madrid, and sandals now symbolize the center of Birkenstock’s product line.

Alongside the way in which, serendipity performed a task within the firm’s growth. In 1966, a Californian named Margot Fraser, when visiting her native Germany, found that Birkenstocks helped her drained and hurting ft, and he or she satisfied Karl Birkenstock to strive promoting the corporate’s sandals in California. It’s mentioned that Karl superior her credit score, and helped her persuade reluctant California retailers to hold the firm’s unconventional footwear of their shops. That proved well timed, since individuals protesting towards the warfare and society’s ills latched on to those sandals, making them them symbolic footwear for the rebellious. within the Nineties, the model had a rebirth, when a really younger Kate Moss wore it for a canopy story, and it turned a sizzling model, particularly on school campuses. Right now, Birkenstock will get greater than 50% of its revenues in the US, with a number of celebrities amongst its prospects. The corporate’s prospectus does a superb job portray an image of each the product choices and buyer base, main into the IPO, and I’ve captured these statistics within the image beneath:

In contrast to some in its designer and model title friends, the corporate’s merchandise usually are not exorbitantly overestimated and the corporate’s greatest vendor, the Arizona, sells for near $100. Whereas the corporate sells extra sneakers to girls than males, it sells footwear to a surprisingly numerous buyer base, when it comes to earnings, with 20% of its gross sales coming from prospects who earn lower than $50,000 a 12 months, and when it comes to age, with virtually 40% of its revenues coming from Gen X and Gen Z members.

For a lot of its historical past, Birkenstock was run as a household enterprise, capital constrained and with restricted development ambitions, maybe explaining its lengthy life. The turning level for the corporate, to get to its present type, occurred in 2012, when the household, dealing with inner strife, turned management of the corporate over to exterior managers, selecting Markus Bensberg, an organization veteran, and Oliver Reichert, a guide, as co-CEOs of the corporate. Reichert, specifically, was a controversial decide since he was not solely an outsider, however one with little expertise within the shoe enterprise, however the selection proved to be impressed. With an help once more from serendipity, when Phoebe Philo exhibited a black mink-lined Arizona on a Paris catwalk in 2012, resulting in collaborations with high-end designers like Dior, the corporate has discovered a brand new life as a development firm, with revenues rising from €200 million in 2012 to greater than €1.4 billion within the twelve months main into the IPO, representing an 18.2% compounded annual development fee over the last decade:

The surge in revenues has been significantly pronounced since 2020, the COVID 12 months, with totally different theories on why the pandemic elevated demand for the product; one is that folks working from house selected the consolation of Birkenstocks over uncomfortable work sneakers. The corporate’s development has include strong profitability, and the desk beneath exhibits key revenue metrics over the past three years:

|

Be aware that the corporate’s working and gross margins, a minimum of within the final two years, match up effectively with the working margins of the big, model title attire & footwear firms that we highlighted within the final part. It could be early to worth model title, however the firm actually has been delivering margins that put it within the model title group.

The robust development since 2020 present a robust foundation for why the corporate is planning its public providing now, however there may be one other issue that will clarify the timing. In 2021, the household bought a majority stake within the agency to L. Catterton, an LVMH-backed personal fairness agency, at an estimated worth in extra of €4 billion Euros. That deal was funded considerably with debt, leaving a debt overhang of near €2 billion, in 2023; the prospectus states that each one of of the corporate’s proceeds from the providing can be used to pay down this debt. That mentioned, the pricing for the providing has elevated since information of it was first floated in July, with €6 billion plus pricing in preliminary reviews rising to €8 billion in early September and to €9.2 billion in the latest information tales. The corporate has picked up anchor traders alongside the way in which, with the Norwegian sovereign fund planning to purchase €300 million of the preliminary providing.

Birkenstock’s Intangibles

Birkenstock is an efficient automobile for figuring out and valuing intangibles, because it has so lots of them, with some extra sustainable and extra helpful than others:

- Model Title: It’s plain that Birkenstock not solely has a model title, when it comes to recognition and visibility, however has the pricing energy and working margins to again up that model title. Nonetheless, as is commonly the case, the constructing blocks that gave rise to the model title are advanced and various. The primary is the distinctiveness of the footwear makes the corporate stand out, with individuals individuals both hating its choices (ugly, clunky, clog) or loving it. In contrast to many footwear firms that try to repeat the most well liked types, Birkenstock marches to its personal drummer. The second is that the corporate’s give attention to consolation and foot well being, in designing footwear, in addition to using high quality substances, is matched by actions. In actual fact, one motive that the corporate makes virtually all of its sneakers nonetheless in Germany, fairly than offshoring or outsourcing, is to protect high quality, and sticks with time-tested and high quality substances, is to protect this status. The third is that not like among the firms on the massive model title record, Birkenstock’s usually are not exorbitantly overestimated, and has a various (when it comes to earnings and age) buyer base. Briefly, its model title appears to have held up effectively over the generations.

- Celeb Buyer Base: As I famous earlier, particularly as Birkenstocks entered the US market, they attracted a celeb clientele, and that has continued by way of right this moment. Birkenstock attracts celebrities in several age teams, from Gwyneth Paltrow & Heidi Klum to Paris Jackson & Kendall Jenner, and extra impressively, it does so with out paying them sponsorship charges. If the perfect promoting is unsolicited, Birkenstock clearly has mastered the sport.

- Good Administration: I have a tendency be skeptical about claims of administration genius, having found that even probably the most extremely regarded CEOs include blind spots, however Birkenstock appears to have struck gold with Oliver Reichert. Not solely has he steered the corporate in the direction of excessive development, however he has carried out so with out upsetting the stability that lies behind its model title. In actual fact, whereas Birkenstock has entered into collaborative preparations with different excessive profile model names like Dior and Manolo Clean, Reichert has additionally turned down profitable presents to collaborate with designers that he feels undermine Birkenstock’s picture.

- The Barbie Buzz: For a corporation that has benefited from serendipitous occasions, from Margot Fraser’s introduction of its footwear to People in 1966 to Phoebe Philo’s sandals on the Paris catwalk in 2012, probably the most serendipitous occasion, a minimum of when it comes to its IPO, might have been the discharge of the Barbie film, this summer time. Margot Robbie’s pink Birkenstock sandals in that film, which has been the blockbuster hit of the 12 months, hyper charged the demand for the corporate’s footwear. It’s true that buzzes fade, however not earlier than they create a income bump and maybe even improve the shopper base for the long run.

For the second, these intangibles are qualitative and fuzzy, however within the subsequent part, I’ll attempt to deliver them into my valuation inputs.

Birkenstock Valuation

My Birkenstock valuation is constructed round an upbeat story of continued excessive development and sustained working margins, with the main points beneath:

- Income Development: The corporate is coming into the IPO, with the wind at its again, having delivered a compounded annual development fee of 18.2% in revenues within the decade main into the providing. That mentioned, its revenues now are €1.4 billion, fairly than the €200 million they have been in 2012, and development charges will come all the way down to replicate the bigger scale. Whereas the typical CAGR in revenues for large model attire & footwear corporations has been 8.66%, I consider that Oliver Reichert and the administration group that runs Birkenstock will proceed their profitable historical past of opportunistic development, and be capable to triple revenues over the following decade. This can be achieved with an help from the Barbie Buzz in 12 months 1 (pushing the expansion fee to 25% over the following 12 months) and a compounded development fee of 15% a 12 months within the following 4 years.

- Profitability: Birkenstock has had a historical past of robust working margins, pushed by its model title and visibility. Within the twelve months main into the IPO, the corporate reported a pre-tax working margin of twenty-two.3%, and its margins over the past decade have hovered round 20%. I consider that the power of the model title will maintain and maybe even barely improve working margins for the corporate, with the margin rising to 23%, over the following 12 months, and to 25% over the next 4 years.

- Reinvestment: Birkenstock has been circumspect in investing for development, over its historical past, exhibiting reluctance to maneuver away from its reliance on its German workforce, and in making acquisitions. It has additionally not been a giant spender on model promoting, utilizing its movie star clientele as a key part of constructing and rising its model I consider that the movie star clientele impact will enable the corporate to proceed on its path of environment friendly development, delivering €2.62 for each euro invested, matching the third quartile of massive model attire corporations.

- Danger: The Catterton acquisition of a majority stake in Birkenstock in 2021 was funded with a major quantity of debt, however the proceeds from the providing are anticipated to be utilized in paying down debt. The corporate ought to emerge from the providing with a debt load on par with different model title attire & footwear firms, and the focus of its manufacturing in Germany will cut back publicity to provide chain and nation danger.

- IPO Proceeds: Information tales recommend that Birkenstock is planning to supply about 21.5 million shares to the general public, and use the proceeds (estimated to be €1 billion, on the €45 providing value) to pay down debt. In conjunction, Catterton plans to promote about the identical variety of shares on the providing as effectively, decreasing its stake within the firm, and cashing out on what ought to be a giant win for the personal fairness participant.

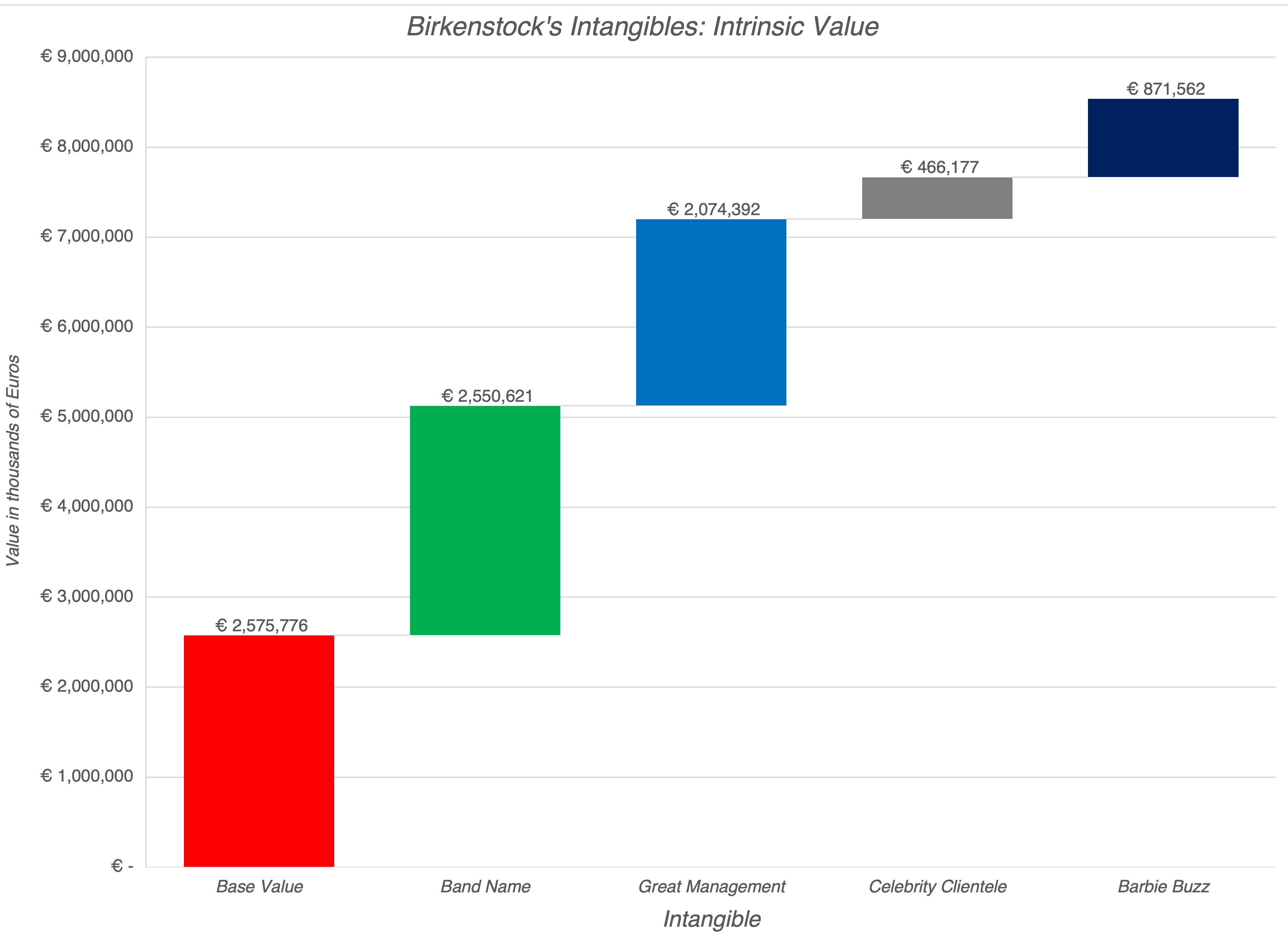

To see how these inputs play out in worth, I’ve introduced them collectively within the (dense) valuation image beneath. With every of the inputs, I’ve highlighted each the numbers that I’m utilizing, in addition to highlighting how a lot intangibles contribute to every enter:

The worth that I estimate for Birkenstock, with my inputs on development, profitability and danger, is about €8.38 billion, about 10% lower than the rumored providing pricing, however nonetheless effectively inside shouting distance of that quantity. In case you’re tempted to make use of the corporate’s many intangibles as the reason for the distinction, observe that I’ve already integrated them into my inputs and worth. To make specific that impact, I’ve remoted every intangible and its impact on worth within the desk beneath:

To worth every intangible, I toggle the enter that displays the intangible on and off to find out how a lot it modifications worth. The intangible that has the most important impact on worth is model title, adopted by the power of the administration group, with the Barbie Buzz and Celeb Results lagging. One other method of visualizing how these intangibles play into worth is to construct as much as estimated worth of fairness of €8.38 billion in items:

These worth judgments are based mostly upon my estimates, and they’re, in fact, open for debate. For example, you may argue that the impact of excellent administration on income development is kind of than my estimate, and even that the consequences spill over into different inputs (price of capital, margins and reinvestment), however that could be a wholesome debate to have.

Pricing Elements

It’s plain that the Birkenstock IPO can be priced, not valued, and the query of how the inventory will do is simply as a lot dependent, maybe extra so, on market temper and momentum, as it’s on the basics highlighted within the valuation.

- Taking a look at information in regards to the firm, the timing works effectively, because the firm is coming into the market on a wave of excellent publicity. Virtually each information story that I’ve learn in regards to the firm paints a optimistic image of it, with laudatory mentions of Oliver Reichert and the corporate’s merchandise, intermixed with footage of not solely Barbie’s pink Birkenstock however a bunch of different celebrities.

- It’s the market temper that’s working towards the corporate, a minimum of for the time being that I’m penning this put up (October 6, 2023). As I wrote in my put up on bipolar markets only a few days in the past, the market temper has soured, with the optimism that we had dodged the bullet that was so broadly prevalent only a few weeks in the past changed with the pessimism that darkish days lie forward for the worldwide economic system and markets.

At its providing pricing of €9.2 billion (€45 to €50 per share), the corporate and its bankers appear to be betting that the nice vibes in regards to the firm will outweigh the unhealthy vibes out there, however that’s gamble. As somebody who has tried and rejected the Arizona sandal, I’m unlikely to be a buyer for Birkenstock footwear, however it is a firm with a really distinctive model title and a administration group that understands the fragile stability between using a model title effectively and overdoing it. It’s, in my opinion, a attain at €45 or €50 per share, but when the market turns bitter, and the inventory drops to beneath €40, I’d be a purchaser.

YouTube Video

Attachments

Wow Thanks for this review i find it hard to search for smart ideas out there when it comes to this material appreciate for the blog post website