On the Cash: Avoiding the Habits Hole with Carl Richards, Might 22, 2024

Why do buyers underperform their very own investments? Why does this occur, and what can we do to keep away from these poor outcomes? In at the moment’s On the Cash, we talk about higher handle the behavioral errors that harm portfolios.

Full transcript beneath.

~~~

About this week’s visitor: Carl Richards is a Licensed Monetary Planner and creator of The New York Occasions Sketch Man column. By his easy sketches, Carl makes advanced monetary ideas straightforward to know. He’s the writer of The Habits Hole: Easy Methods to Cease Doing Dumb Issues with Cash.

For more information, see:

~~~

Discover the entire earlier On the Cash episodes right here, and within the MiB feed on Apple Podcasts, YouTube, Spotify, and Bloomberg.

TRANSCRIPT: Carl Richards

[Musical Intro: Ain’t misbehaving, saving all my love for you]

Barry Ritholtz: What number of occasions has this occurred to you? Some fascinating new fund supervisor or ETF is placing up nice numbers, generally for years, and also you make the leap and at last purchase it. It’s a scorching fund with super efficiency, however after a number of years, you evaluation your portfolio and surprise, hey, how come my returns aren’t almost nearly as good as anticipated?

You could be experiencing what has change into often called the conduct hole. It’s the rationale your precise efficiency is far worse than the fund you buy.

I’m Barry Ritholtz, and on at the moment’s version of At The Cash, we’re going to debate keep away from affected by the conduct hole.

To assist us unpack all of this and what it means to your portfolio, let’s usher in Carl Richards. He’s the writer of The Habits Hole, Easy Methods To Cease Doing Dumb Issues With Cash. The guide focuses on the underlying behavioral points that lead folks to make flawed choices. Poor monetary choices.

So Carl, let’s simply begin with a primary definition. What’s the conduct hole?

Carl Richards: Thanks Barry. Tremendous enjoyable to talk with you about this. That is going again now 20 years, proper? Like I simply stumbled upon this early on in my work with buyers. That we’d get all excited. I’d get all excited! Precisely as you stated like we’d do some efficiency evaluation, we’d discover some enjoyable. We thought was nice. After all, previous efficiency is not any indication of future outcomes.

However what’s the very first thing you have a look at? [past performance] While you resolve to make yeah previous efficiency get all enthusiastic about it After which you’ve gotten this inevitable letdown and so I feel the simplest option to describe that is think about you open the newspaper; and, uh, there’s an, there’s a commercial. Keep in mind the quaint newspaper, proper? There’s an commercial for a mutual fund that claims 10-year common annual return of 10%.

Properly, that’s the funding return. And I feel all of us overlook that investments are completely different than buyers. And so the conduct hole is the distinction between the funding return and the return you, uh, earn as an investor in your account. And that’s, My expertise and the info present that always particular person buyers underperform the common funding.

So this nicely intentioned conduct of discovering the most effective funding is producing a suboptimal end result for us as buyers.

Barry Ritholtz: So what’s the underlying foundation for that hole? I’m assuming, particularly if we’re speaking a few scorching fund, the fund has had an ideal run up folks by if not the highest, nicely definitely after it’s had an enormous transfer after which a little bit little bit of imply reversion comes again into it.

The fund does poorly for a few years after which form of goes again to the place it was. Is it simply so simple as shopping for excessive and, and being caught with it low? Is, is it that straightforward?

Carl Richards: Yeah, I, it’s fascinating. Let me simply inform you a fast story. And that is about all, all nice funding tales are about your father-in-law, proper? So I keep in mind my father-in-law in ’97, ’98, ’99. He had an funding advisor. His advisor was named Carter. I keep in mind all this. And he owned, and I can title particular funds as a result of this stuff will not be the issue, the fund didn’t make the error, proper? So, Alliance Premier Development, if you happen to keep in mind, 97, 98, 99, simply, you understand, he owned Alliance Premier Development, and he owed Davis Worth Fund, so go-go development fund, and one thing that was classically worth.

And on the finish of ’97, he appears at his returns and he’s like, why can we personal this? Then this Davis, this worth fund, why can we personal this factor? Carter talks him into rebalancing, which implies he took some from Alliance premier development, moved it to Davis reverse of what he felt like doing. Proper.

98 comes round. Similar factor. The Alliance premier development knocks it out of the park. Davis solely does like 12 p.c or one thing. Proper. Father in legislation complains. Carter says, hey, please, come on. Like, that is simply, that is simply what we do. We’re really going to do the alternative of what you’re feeling. We’re going to promote some Alliance Premier Development, we’re going to rebalance into Davis. ‘99, proper? And I can’t recall the precise numbers, but when Alliance did one thing like 54%. And Davis solely did 17%.

And my father in legislation was like, that’s it. That’s it. And I keep in mind New Yr, like over Christmas, over the Christmas vacation of 99. Proper. And you understand what occurs subsequent?

He tells me, he’s like, yeah, I lastly had sufficient. I fired these Davis, that Davis New York enterprise fund and moved all the cash to Alliance premier development simply in time. You recognize, now we have one other, he felt like a hero for January, February, after which March of 2000, simply in time to get his head taken off. And we repeat that time and again.

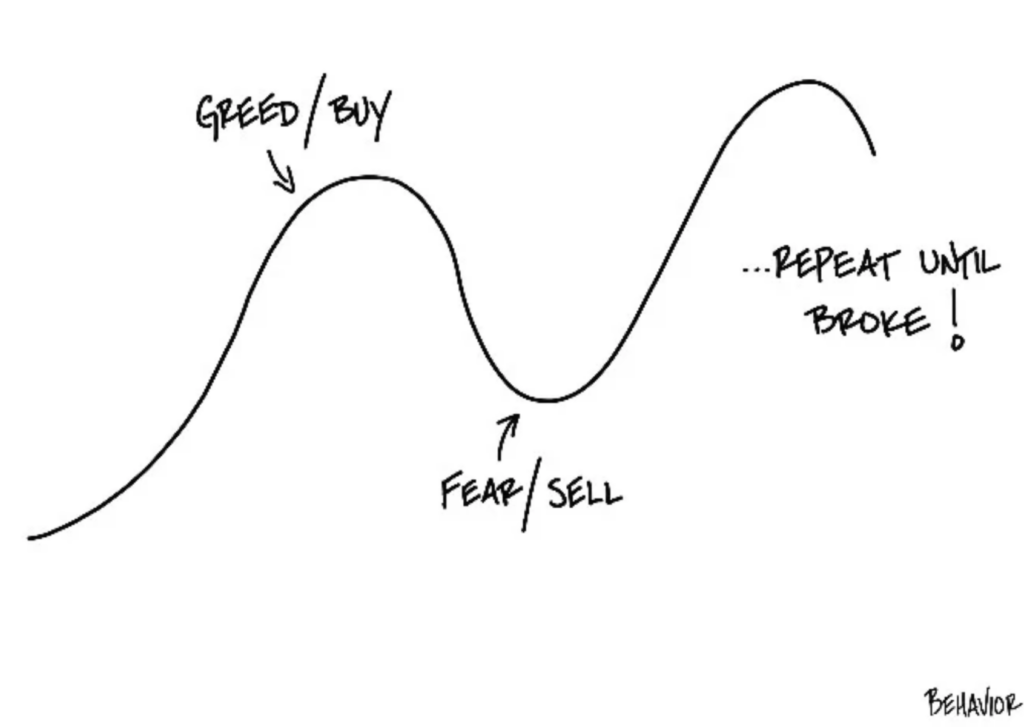

And it’s, it’s form of wired into us. So it’s, it’s difficult. You need extra of what provides you safety or pleasure. And also you wish to run away from issues that trigger you ache as quick as attainable. And in some way we’ve translated that into purchase excessive and promote low and repeat till broke.

Barry Ritholtz: And I occur to have, the quantity one in all that sequence of lithographs you probably did. Repeat till broke. Hanging in my workplace.

And, and let’s put a little bit, a little bit meat on the bones, if you happen to, if you happen to had been closely invested in any fund that was closely uncovered to the NASDAQ, from the height in March 2000 to only two years later by October of 02, the NASDAQ was down about 81 p.c peak to trough.

Yeah. That’s a hell of a haircut dropping 4 fifths of, of the worth.

Carl Richards: Particularly simply I imply I keep in mind these conversations like there was I imply that is form of enjoyable to poke enjoyable at your father-in-law, proper, but it surely wasn’t very enjoyable when there was like some fairly main drastic modifications in the way in which the household was working Due to that have prefer it was it was an actual deal for many folks, proper?

And Barry simply to level out like that was not Funding mistake. That was an investor mistake, proper? In case you had simply caught to the plan, which is rebalance annually, you’d have been high-quality. It will have been painful, however not almost as painful because it turned out to be.

Barry Ritholtz: And I’d guess the Davis Worth Fund did fairly nicely within the early 2000s, definitely relative to the expansion fund.

Carl Richards: For positive. You’ll have been defending that. You’ll have been systematically Shopping for comparatively low and promoting comparatively excessive alongside the way in which, systematically, as a result of it’s simply what you do, and that’s referred to as rebalancing.

Barry Ritholtz: So, the conduct hole creates this area between how the funding performs and the way the investor performs how large can that hole get how giant?

Does the conduct hole between precise fund efficiency and investor returns change into?

Carl Richards: Yeah, that is actually problematic as a result of there are a few completely different research and none of them are nice. My expertise with it’s extra anecdotal like experiences. I’ve just like the story I simply informed I might inform 20 of these tales You Proper.

Given, I imply, did anyone listening change into an actual property investor in ‘07, proper? Like over, uh, you understand, we, we don’t must even go into the, Crypto NFT scenario, proper? However simply time and again we do it, however Morningstar numbers, I feel are my favourite and that at all times places it round a 1%, a p.c and a half over lengthy durations of time. Which once we’re all scraping for 25 foundation factors, you understand, operating round making an attempt to eke out the final little bit of return, then this conduct hole that prices us some extent to some extent and 1 / 4 is one thing value taking note of.

Barry Ritholtz: Yeah, particularly as, as how that’s compounded over time, it will possibly actually add as much as one thing substantial. So let’s discuss the place the conduct hole comes from. It seems like our feelings are concerned. It seems like concern and greed is what Drives the conduct hole inform inform us what you discovered.

Carl Richards: Yeah, it’s humorous once I initially discovered this, I felt like this was a discovery, (you understand cute of me) as a result of a number of different folks have been writing about It for years. I used to be making an attempt to place a reputation on this hole and I referred to as it initially the “Emotional hole” I’m actually glad I modified the title to the conduct hole for the guide however to me there was simply I couldn’t clarify it apart from or investor conduct and I feel You Once we perceive how we’re wired and I can’t keep in mind who was it Buffett that stated after all We might simply we are able to at all times attribute it to Buffett if it was good, but it surely was “If you wish to design a poor investor, design a human.” proper?

We’re hardwired and it’s stored us alive as a species: To get extra of the stuff that’s giving us safety or pleasure and to run as quick as we are able to Like I don’t actually care. I don’t care what you inform me if my hand’s on a burning range, I’m gonna take it off. Throw all of the information and figures you need at me.

Attempt to be rational with me all day lengthy. I’m, I’m taking my hand off. And in some way, particularly given the form of circus that exists round investing, you understand, the place you bought folks yelling and screaming, purchase, promote, purchase, promote all day lengthy. We translate market down, market down. Oh no, if I don’t do one thing and we challenge the current previous and positively sooner or later, and I’ve seen folks really do the calculations.

If the final two weeks proceed. In 52 weeks, I’m going to don’t have any cash left. [the market’s going to zero!] Yeah. We’ve this recency bias drawback. We’ve being hardwired for safety and pleasure. We’ve security herd conduct. When all of your neighbors are yelling, proper. It’s actually laborious to not you understand,

It was a Buffett quote, proper? “I wish to be grasping when everyone else is fearful and fearful when everyone else is grasping” and that’s cute to say. However while you’ve really been punched within the face, you behave a little bit otherwise, proper?

Barry Ritholtz: So the opposite factor that I observed that you just’ve written about relating to the conduct hole is how a lot we concentrate on points which are utterly out of our management.

What’s occurring with markets going up and down? Who’s Russia invading? What’s occurring within the Center East? When’s the Fed going to chop or elevate charges? All of this stuff are utterly exterior of not solely our management, however our skill to forecast. What ought to buyers be specializing in as a substitute?

Carl Richards: Yeah, I feel portfolio building, when finished appropriately, it takes into consideration the weighty proof of historical past, and the weighty proof of historical past consists of all of these occasions that we couldn’t have forecasted earlier than.

So we shouldn’t be shocked that issues that we didn’t take into consideration will present up subsequent 12 months and subsequent week. And people issues that we didn’t take into consideration may have the best influence on our portfolio. So it’s actually just like the unknown unknowns that may have the best influence. We’ll design the portfolio with that in thoughts.

Properly, how do you do this? We’ll use the weighty proof of historical past as a result of it’s been occurring for a very long time. So I feel the way in which to concentrate on what, just like the factor you’ll be able to management essentially the most is portfolio building, asset allocation, and prices. Like if we simply get clear about that. The portfolio is designed.

Right here’s a query to ask you. I’ve been asking this query as like a a sport for the final 5 years. Why is your portfolio constructed the way in which it’s? And the commonest reply is, like I heard about it on the information, the actually good folks whisper, “I examine it in The Economist.” Proper? However the appropriate reply is, this portfolio is designed deliberately to provide me the best probability of assembly my very own objectives. Properly, these are the issues you’ll be able to concentrate on.

Barry Ritholtz: Fairly intriguing. So to wrap up, when buyers chase scorching funds or ETFs or sectors or no matter is the flavour of the second, there’s a bent to purchase excessive, and if subsequently they get out of those buys, positions or promote right into a panic or market correction, they’re all however assured to generate a efficiency worse than the fund itself.

To keep away from succumbing to the conduct hole, you could study to handle your individual conduct. I’m Barry Ritholtz, and this has been Bloomberg’s At The Cash.

[Musical Outro: Ain’t misbehaving, saving all my love for you]

~~~