For those who now not want a bank card, your instinct would let you know to cancel it. Lower up the cardboard and toss the items within the trash.

However canceling a card can decrease your credit score rating due to how the credit score rating calculation.

For those who now not want a bank card, right here’s how one can safely cope with it with out placing any strain in your credit score or credit score rating.

Desk of Contents

We’ll first go into the strategies for safely canceling a card after which clarify why you must take these measures.

Steps to Safely Cancel a Credit score Card

1. Think about Sticking it in a Secure Place

I by no means cancel a bank card due to the way it can decrease your credit score rating so when you’re snug with the thought, simply depart the cardboard open however put it in a protected place. This retains the road open in your report and your credit score restrict as excessive as potential, so your utilization stays decrease.

Then, ensure you use the cardboard each few months in order that the issuer doesn’t cancel it for inactivity. it doesn’t matter in the event that they cancel it otherwise you do, the adverse influence is similar.

2. Redeem Rewards

When you have any excellent rewards on the bank card you need to shut, and also you don’t use them earlier than you shut the account, there’s probability these rewards might be forfeited. Generally, if the rewards are by a distinct firm, reminiscent of a lodge or airline, you may maintain them as a result of they’re tied to the lodge or airline and never the bank card.

To keep away from all this, simply use use the rewards. Discover out if the bank card firm will reduce you a examine or what the process is to get your rewards steadiness.

Then comply with these procedures earlier than you shut the cardboard. If you need to anticipate a sure timeline to be met earlier than you will get your rewards, clarify your scenario and ask if you will get them early since you need to shut the cardboard.

If the bank card firm refuses to subject your rewards early, it’s possible you’ll need to wait on closing the cardboard till you may redeem the rewards.

3. Pay Off Excellent Balances

After you’ve taken care of getting any rewards, it’s a good suggestion to repay the cardboard in full. This isn’t required but it surely’s a good suggestion since when you shut the account the financial institution has no cause to increase any courtesies, reminiscent of waiving a payment or reducing your rate of interest.

First, name the bank card firm to get the present payoff quantity. Don’t go off your most up-to-date bank card assertion or your on-line steadiness as there could be curiosity that’s due however not but utilized to that steadiness.

Due to this fact, name and get the payoff steadiness and discover out what date it’s good by. Then pay the steadiness in full earlier than the required due date.

That means you remove any chance of closing a card and leaving an unpaid steadiness that might have an effect on your credit score unbeknownst to you.

4. Ask to Have the Account Downgraded or Closed

Right here’s the place there’s a little bit of “credit score rating technique” comes into play.

If you wish to shut a bank card since you don’t need to pay an annual payment, you may ask the bank card firm to “downgrade” your card to 1 with out an annual payment. This maintains your restrict and doubtlessly the credit score line’s historical past whereas additionally eradicating an annual payment.

That is when the bank card issuer might supply to waive the annual payment, which solves your payment drawback, or they downgrade you, which once more solves your payment drawback.

If they’ll’t do both, otherwise you’re set on cancelling the cardboard, then closing is the way in which to go.

Name the quantity on the again of the bank card for steering. For those who don’t have the cardboard, you’ll find the quantity in your assertion or on-line.

Throughout your name, remember to ask the bank card firm in the event that they’ll mail out a verification letter concerning the cardboard closing. Some firms may not do this, however most will.

5. Affirm Closure on Your Credit score Report

About six weeks after you’ve closed the account, you’ll need to examine your credit score report to make sure the cardboard was certainly closed simply to make certain.

You may go to AnnualCreditReport.com to get your credit score experiences from every of the bureaus every week.

While you’ve gotten your report, examine and see that the account for the cardboard you’ve closed does certainly mirror that it’s closed. Doing so will assist forestall any fraudulent exercise on the cardboard sooner or later.

So, how does canceling or closing a card have an effect on your rating?

How Cancelling Can Have an effect on Your Credit score Rating

When speaking about how one can cancel a bank card safely, you is perhaps questioning what the massive deal is. In spite of everything, it’s not just like the issuing financial institution of stated bank card will hunt you down, forcing you to make use of the cardboard “or else.”

Right here’s the way it can influence your rating:

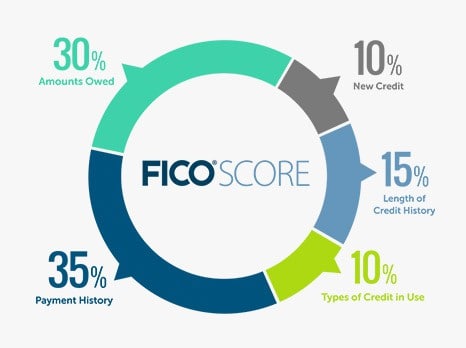

Your Credit score Utilization Ratio (Quantities Owed)

A Credit score Utilization Ratio is an vital think about your credit score rating – it accounts for 30% of your FICO credit score rating. Your credit score utilization ratio is decided by dividing the quantity of bank card debt you’ve got by the whole accessible credit score you’ve got.

In case your whole bank card limits is $20,000 and you’ve got excellent bank card balances of $10,000, you’ve got a credit score utilization ratio of fifty%. For those who pay these bank card balances all the way down to $5,000, your credit score utilization ratio drops all the way down to 25%.

Credit score reporting companies wish to see an individual’s credit score utilization ratio at 30% or much less.

Now, let’s take that very same situation assuming you’ve received the $5,000 in bank card debt and $20,000 of whole bank card limits. Your ratio is 25%.

For those who shut a bank card with a $10,000 restrict and are left with $10,000 in whole bank card limits, your ratio will then rise to 50%.

And that leaves a possible to drop your credit score rating as a result of it seems such as you’re utilizing a bigger portion of your accessible credit score, when, in truth, your excellent bank card balances are the identical.

Your Fee Historical past

One other means closing a bank card in a dangerous method can harm you has to do together with your cost historical past, which accounts for 35% of your rating. If the bank card you’re contemplating closing is one that you simply’ve held for a few years, cost historical past on the cardboard is a optimistic think about your good credit score rating.

For those who shut that card and are solely left with playing cards that haven’t been opened for very lengthy, it will probably seem as in case your credit score utilization historical past is shorter than it truly is.

The rating additionally elements into the typical age of your credit score strains so in some circumstances, canceling a more moderen card might have a small optimistic profit however that is usually rarer.