I’ll begin this publish with a few confessions. The primary is that my portfolio has held up nicely this 12 months, in a market that has been top-heavy and tech-driven, and one large purpose is that it incorporates each NVIDIA and Microsoft, two corporations which have benefited from the AI story. The second is that a lot as I want to declare credit score for foresight and ahead considering, AI was not even a speck in my creativeness once I purchased these shares (Microsoft in 2014 and NVIDIA in 2018). I simply occurred to be in the suitable place on the proper time, a reminder once more that being fortunate typically beats being good, no less than in markets. That mentioned, NVIDIA’s hovering inventory worth has left me going through that query of whether or not to money out, or let my cash experience, and thus requires an evaluation of how the promise of AI play’s out in its worth. Alongside the way in which, I’ll check out the promise of AI, in addition to the perils for buyers, drawing on classes from the previous.

The Semiconductor Enterprise

The semiconductor enterprise, in its present type, had its progress spurt as a consequence of the PC revolution of the Nineteen Eighties, as private computer systems transitioned from instruments and playthings for geeks to on a regular basis work devices for the remainder of us. Within the final 4 a long time, pc chips have turn into a part of nearly all the pieces we use, from home equipment to cars, and the businesses that manufacture these chips have seen their fortunes rise, and typically be put in danger, as know-how shifts.

1. From Excessive Development to Maturity!

It was the private pc enterprise within the Nineteen Eighties that gave the semiconductor enterprise, as we all know it, its increase, and as know-how has more and more entered each side of life, the semiconductor enterprise has grown. To map the expansion, I began by trying on the aggregated revenues of all international semiconductor corporations within the chart beneath from 1987 to 2023 (via the primary quarter):

|

| Supply: Semiconductor Business Affiliation |

From near nothing firstly of the Nineteen Eighties, revenues at semiconductor corporations surged within the Nineteen Eighties and Nineties, first boosted by the PC enterprise after which by the dot-com increase. From 2001 to 2020, income progress at semiconductor companies has dropped to single digits, as larger demand for chips in new makes use of has been offset by lack of pricing energy, and declining chip costs. Whereas income progress has picked up once more within the final three years, the enterprise has matured.

2. Sustained Profitability, with Cycles!

The semiconductor enterprise has typically been a worthwhile one for a lot of its existence, as could be seen within the mixture margins of corporations within the enterprise beneath:

Whereas gross and working margins have at all times been wholesome, the decide up in each metrics since 2010 is a testimonial to the upper profitability in some segments of the chip enterprise, whilst competitors commoditized different segments. As could be seen within the periodic dips in profitability throughout time, there are cycles of profitability which have continued, even because the enterprise has matured.

It’s price noting that these margins are understated, due to the accounting therapy of R&D as an working expense, as a substitute of as a capital expenditure. The R&D adjusted working margin at semiconductor corporations is larger by about 2-4%, in each time interval, with the adjustment to working taking the type of including again the R&D expense from the 12 months and subtracting out the amortization of R&D bills over the prior 5 years (utilizing straight line amortization).

3. Love-Hate Relationship with Markets!

Because the semiconductor enterprise has acquired heft, when it comes to revenues and profitability, buyers have priced these working outcomes into the market capitalization assigned to those corporations. Within the graph beneath, I report the collective enterprise worth and market capitalization of worldwide semiconductor corporations, said in US greenback phrases:

As you’ll be able to see, the semiconductor corporations have loved lengthy intervals of glory, interspersed with intervals of ache in markets, beginning with a decade of surging market capitalizations within the Nineties, adopted by a decade within the wilderness, with stagnant market capitalization, between 2000 and 2010, earlier than one other decade of progress, with market capitalizations surged six-fold between 2011 and 2020. Be aware that for essentially the most half, semiconductor corporations carry mild debt hundreds, resulting in enterprise values that both path in market capitalization in some years (as a result of money exceeds debt) or are very near market capitalization in different years (as a result of web debt is near zero).

As market capitalizations have risen and fallen, the a number of of revenues that semiconductor corporations has additionally fluctuated, reaching a excessive within the dot-come period, with semiconductor corporations buying and selling collectively at greater than seven occasions revenues to an extended stretch the place they traded at between two and 3 times revenues, earlier than spiking once more between 2019 and 2021. If costs are a mirrored image of what the market thinks concerning the future, the pricing of semiconductor corporations appears to point an acceptance on the a part of buyers that the enterprise has matured.

4. Shifting Solid of Winners and Losers!

Because the semiconductor enterprise has matured, it has additionally modified when it comes to each the largest gamers within the enterprise, in addition to the biggest clients for its merchandise . Within the desk beneath, we present the evolution of the highest ten semiconductor corporations, when it comes to revenues, from 1990 via 2023, at ten-year intervals:

The forged of gamers has modified over time, with solely two corporations from the 1990 checklist (Intel and Texas Devices) making it to the 2023 checklist. Over the a long time, the Japanese corporations on the checklist have slipped down or disappeared, to get replaced by Korean and Taiwanese corporations, with Taiwan Semiconductors being the largest mover, shifting to the highest of the checklist in 2022. After an extended stretch on the high, Intel has dropped again down the checklist and ranked third, when it comes to revenues, in 2022. Be aware that NVIDIA, the topic of this publish, was eighth on the checklist in 2023, and has remained at that rating from 2010. That will appear at odds with its rising market capitalization however it’s indicative of the corporate’s technique of going after area of interest markets with excessive profitability, quite than attempting to develop for the sake of progress.

The purchasers for semiconductor chips have additionally modified over time, with the shift away from private computer systems to smartphones, with demand rising from vehicle, crypto and gaming corporations within the final decade. Over the previous couple of years, information processing has additionally emerged as demand driver, and it’s protected the say that increasingly more of the worldwide economic system is pushed by pc chips:

|

| Semiconductor Business Affiliation |

The forecasts for the longer term (2030), have been for quicker progress in vehicle and {industry} electronics, however the potential surge in demand from AI merchandise was largely underplayed, displaying how shortly market forecasts could be subsumed by adjustments on the bottom.

NVIDIA: The Opportunist!

NVIDIA was based in 1993 by Jensen Huang, however it remained a distinct segment participant till the early elements of this century. A lot of its rise has come within the final decade, simply as revenues for the general semiconductor enterprise have been beginning to degree off, and on this part, we’ll look via the corporate’s historical past, on the lookout for clues to its success and present standing.

1. Opportunistic Development, with Profitability

NVIDIA went public in January 22, 1999, with the dot-com increase nicely beneath method, and its inventory worth popped by 64% on the providing date. On the time of its public providing, the corporate was money-making, however with small revenues of $160 million, making it a bit participant within the enterprise. As you’ll be able to see within the graph beneath, these revenues grew between 2000 and 2005, to achieve $2.4 billion in 2005. Within the following decade (2006-2015), the annual income progress charge dropped again to 7-8% a 12 months, however that progress allowed the corporate to make the highest ten checklist of semiconductor corporations by 2010. Effectively-timed bets on gaming and crypto created a surge within the income progress charge to 27.19% between 2016-2020, and that progress has continued into the final two years:

There are two spectacular elements to NVIDIA’s historical past. The primary is that it has been capable of keep spectacular progress, even because the {industry} noticed a slowing of income progress (3.97% between 2011-2020). The second is that this excessive income progress has been accompanied not simply with earnings, however with above-average profitability, as NVIDIA’s gross and working margins have run forward of {industry} averages. NVIDIA has clearly embraced a technique of investing forward of, and going after, progress markets for the chip enterprise, and that technique has paid off nicely. Thus, its present dominant positioning within the AI chip enterprise could be considered as extra proof of that technique at play.

There’s one ultimate part to NVIDIA’s enterprise mannequin that wants noting, each from a profitability and threat perspective. NVIDIA ‘s core enterprise is constructed round analysis and chip design, not chip manufacturing, and it outsources nearly all of its chip manufacturing to TSMC. Its margins then come from its capability to mark up the costs of those chips and it’s uncovered to the dangers that any future China-Taiwan tensions can disrupt its provide chain.

2. Giant, albeit Productive Reinvestment

Whereas NVIDIA’s progress and profitability have been spectacular, the worth cycle is just not full till you carry within the funding that the corporate has needed to make to ship that progress. With a semiconductor firm, that reinvestment contains not solely investing in manufacturing capability, but in addition within the R&D to create the following era of chips, when it comes to energy and functionality. As with the sector, I capitalized R&D at NVIDIA, utilizing a 5-year life, and recalculated my working earnings (for the reason that reported model is constructed on the accounting mis-reading of R&D as an working expense). That ends in a corrected model of pre-tax working margin for NVIDIA that was 37.83% and a pre-tax return on capital of 24.42% in 2021-2023:

I additionally computed a gross sales to capital ratio, measuring the {dollars} of gross sales for every greenback of capital invested. In 2022, that quantity, for NVIDIA, was 0.65, indicating that that is positively not a capital-light enterprise and that NVIDIA has invested closely to get to the place it’s at present, as an organization.

3. With a Mega Market Payoff

NVIDIA’s success on the working entrance has impressed monetary markets, and its rise in market capitalization from its IPO days to a trillion-dollar worth could be seen beneath:

I do know that there are lots of who’re regretting their lack of foresight, in not proudly owning NVIDIA via its total run, however acknowledge that this was not a easy experience to the highest. In actual fact, the corporate had near-death experiences, no less than in market worth time period, in 2002 and 2008, dropping greater than 80% of its market worth. That mentioned, I owe my fortunate run with NVIDIA to a kind of downturns in 2018, when the corporate misplaced greater than 50% of its market worth, and it’s a lesson that I hope will come via this chart. Even the largest winners out there have had intervals when buyers have turned intensely unfavourable on their prospects, making them enticing as investments for value-focused buyers.

AI: From Promise to Earnings

Since a lot of the run-up in NVIDIA in the previous couple of months has come from discuss AI, it’s price taking a detour and inspecting why AI has turn into such a robust market driver, and maybe trying on the previous for steerage on the way it will play out for buyers and companies.

Revolutionary or Incremental Change?

I’m sufficiently old to be each a believer and a skeptic on revolutionary adjustments in markets, having seen main disruptors play out each in my private life and my portfolio, beginning with private computer systems within the Nineteen Eighties, the dot-com/on-line revolution within the Nineties, adopted by smartphones within the first decade of this century and social media within the final decade. What set these adjustments aside was that they not solely affected broad swathes of companies, some positively and a few adversely, however that in addition they modified the ways in which we reside, work and work together. In parallel, we’ve got additionally seen adjustments which might be extra incremental, and whereas vital of their capability to create new companies and disruption, do not fairly qualify as revolutionary. I will not declare to have any particular abilities in with the ability to distinguish between the 2 (revolutionary versus incremental), however I’ve to maintain attempting, since failing to take action will end in my dropping perspective and making investing errors. Thus, I used to be unable to share the assumption that some appeared to have concerning the “Cloud” and “Metaverse” companies being revolutionary, since I noticed them extra as extra incremental than revolutionary change.

So, the place does AI fall on this spectrum from revolutionary to incremental to minimalist change? A 12 months in the past, I might have put it within the incremental column, however ChatGPT has modified my perspective. That was not as a result of ChatGPT was on the slicing fringe of AI know-how, which it’s not, however as a result of it made AI relatable to everybody. As I watched my spouse, who teaches fifth grade, grapple with college students utilizing ChatGPT to do homework assignments. and with my very own college students asking ChatGPT questions on valuation that they’d have requested me instantly, the potential for AI to upend life and work is seen, although it’s troublesome to separate hype from actuality.

Enterprise Results

If AI is revolutionary change and will likely be a key market driver for this decade, what does this imply for buyers? Wanting again on the revolutionary adjustments from the final 4 a long time (PCs, dot-com/web, smartphones and social media), there are some classes which will have software to the AI enterprise.

- A Internet Optimistic for Markets? Does revolutionary change assist the general economic system and/or fairness markets? The outcomes from the final 4 a long time is blended. The PC-driven tech revolution of the Nineteen Eighties coincided with a decade of excessive inventory market returns, as did the dot-com increase within the subsequent decade, however the first decade of this century was one of many worst in market historical past as inventory costs flatlined. Shares did nicely once more during the last decade, with know-how as the large winner, and over the 4 a long time of change (1980-2022), the annual return on shares has been marginally larger than within the 5 a long time prior.

Given fairness market volatility, 4 a long time is a short while interval, and essentially the most that we are able to discern from this information is that the technological adjustments have been a web optimistic, for markets, albeit with added volatility for buyers. - With a couple of Large Winners and Numerous Wannabes and Losers: It’s indeniable that every of the revolutionary adjustments of the final 4 a long time has created winners inside the house, however a couple of caveats have additionally emerged. The primary is that these adjustments have given rise to companies the place there are a couple of large winners, with a couple of corporations dominating the house, and we’ve got seen this paradigm play out with software program, on-line commerce, smartphones and social media. The second is that the early leaders in these companies have typically fallen to the wayside and never turn into the large winners. Lastly, every of those companies, profitable although they’ve been within the mixture, have seen greater than their share of false begins and failures alongside the way in which. For buyers, the lesson must be that investing in revolutionary change, forward of others out there, doesn’t translate into excessive returns, for those who again the unsuitable gamers within the race, or extra importantly, miss the large winners. It’s true that at this very early stage of the AI recreation, the market has anointed NVIDIA and Microsoft as large winners, however it’s fully attainable {that a} decade from now, we will likely be completely different winners. On the stage of the hype cycle, it’s also true that just about each firm is attempting to put on the AI mantle, simply as each firm within the Nineties aspired to have a dot-com presence and lots of corporations claimed to have “user-intensive” platforms within the final one, As buyers, separating the wheat from the chaff will solely get harder within the coming months and years, and it’s a part of the educational course of. To the argument that you may purchase a portfolio of corporations that can profit from AI and earn cash from the few that succeed, previous market expertise means that this portfolio is extra more likely to be over than beneath priced.

- With Disruption: The market is affected by the carcasses of what was profitable companies which were disrupted by technological change. Traders in these disrupted corporations not solely lose cash, as they get disrupted, however worse, make investments much more in them, drawn by their “cheapness”. This occurred, simply to supply two examples, with buyers in the brick-and-mortar retail corporations that have been devastated by on-line retail, and with buyers within the newspaper/conventional advert corporations that have been upended by internet marketing. If AI succeeds in its promise, will there be companies which might be upended and disrupted? After all, however we’re within the hype part, the place rather more will likely be promised than could be delivered, however the greatest targets will come into focus sooner quite than later.

The underside line is that even when all of us agree that AI will change the way in which companies and people behave in future years, there isn’t a low-risk path for buyers to monetize this perception.

Worth Results

If historical past is any information, we’re within the hype part of AI, the place it’s oversold as the answer to simply about each downside recognized to man, and used to justify massive worth premiums for the businesses in its orbit, with none try and quantify and again up these premiums. The first argument that will likely be utilized by these promoting these AI premiums is that there’s an excessive amount of uncertainty about how AI will have an effect on numbers sooner or later, an argument that’s at odds with paying numbers up entrance for these expectations. In brief, if you’re paying a excessive worth for an AI impact in an organization, it behooves you to place apart your aversion to creating estimates, and use your judgment (and information) to reach on the impact of AI on cashflows, progress and threat, and by extension, on worth.

In making these estimates, it does make sense to interrupt down AI corporations based mostly upon what a part of the AI ecosystem they inhabit, and I might recommend the next breakdown:

- {Hardware} and Infrastructure: Each main change over the previous couple of a long time has introduced with it necessities when it comes to {hardware} and infrastructure, and AI is not any exception. As you will note within the subsequent part, the AI impact on NVIDIA comes from the elevated demand for AI-optimized pc chips, and as that market is anticipated to develop exponentially, the businesses that may seize a big share of this market will profit. There are undoubtedly different investments in infrastructure that will likely be wanted to make the AI promise a actuality, and the businesses which might be on a pathway to delivering this infrastructure will acquire, as a consequence.

- Software program: AI {hardware}, by itself, has little worth except it’s twinned with software program that may make the most of that computing energy. This software program can take a number of kinds, from AI platforms, chatbots, deep studying algorithms (together with picture and voice recognition, in addition to pure language processing) and machine studying, and whereas there may be much less type and extra uncertainty to this a part of the AI enterprise, it doubtlessly has a lot better upside than {hardware}, exactly for a similar purpose.

- Knowledge: Since AI requires immense quantities of information, there will likely be companies that can acquire worth from gathering and processing information particularly for AI purposes. Large information, used extra as a buzzword than a enterprise proposition, during the last decade might lastly discover its place within the worth chain, when twinned with AI, however that pathway is not going to be linear or predictable.

- Purposes: For corporations which might be extra customers of AI than its purveyors, the promise of AI is that it’s going to change the way in which they do enterprise, with optimistic and unfavourable implications. The most important pluses of AI, no less than as introduced by its promoters, is that it’s going to permit corporations to cut back prices (primarily by changing handbook labor with AI-driven purposes) and make them extra environment friendly, and by extension, extra worthwhile. Even when I concede the primary declare (although I feel that the AI replacements will likely be neither as environment friendly nor as cost-saving as promised), I’m much more cautious of the second declare for a easy purpose. If each firm has AI, and AI reduces prices and will increase effectivity as promised for all of them, it’s way more probably that they may find yourself with decrease costs for his or her merchandise/companies and never larger earnings. On the threat of repeating certainly one of my favourite sayings, “If everybody has it, nobody does” and it’s the foundation for my argument that AI, if it succeeds, will make corporations much less worthwhile, within the mixture. The opposite minus of AI is that if it delivers on even a portion of its promise of automating points of enterprise, it will likely be damaging and maybe even devastating for current corporations that derive their worth presently from delivering these companies for profitable charges. In these companies, AI is not going to simply be a zero-sum recreation, however a negative-sum one.

On the particular questions of how AI will have an effect on investing, typically, and lively investing, in particular, I imagine that whether it is used as a instrument, it may well enrich valuation and investing, and I sit up for with the ability to develop valuation narratives and numbers, with its support. For many who are lively buyers, people in addition to establishments, I imagine that AI will make a troublesome recreation (delivering extra returns or alpha from investing) much more so. Any edge you could have as an lively investor will likely be extra shortly replicated in an AI world, and to the extent that AI instruments will likely be accessible and out there to each investor, by itself, AI is not going to be a sustainable edge for any lively investor.

Social Results

Will AI make our lives simpler or harder? Extra typically, will it make the world a greater or worse place to inhabit? I do know that there are some advocates of AI who paint an image of goodness, the place AI takes over the menial duties that presumably trigger us boredom and brings an unbiased eye to information evaluation that result in higher choices. I do know that there are others who see AI as an instrument that large corporations will use to manage minds and purchase energy. With the expertise of the large adjustments which have engulfed us in the previous couple of a long time nonetheless contemporary, I might argue that they’re each proper. AI will likely be a plus is a few occupations and points of our lives, simply as it is going to create unintended and hostile penalties in others.

There are some who imagine that AI could be held in examine and made to serve its extra noble impulses, by proscribing or regulating its improvement, however I’m not as optimistic for a lot of causes. First, I imagine that each regulators and legislators are woefully incapable of understanding the mechanics of AI, not to mention go smart restrictions on its utilization, and even when they do, their motives aren’t altruistic. Second, any regulation or legislation that’s aimed toward stopping AI’s excesses will nearly definitely set in movement unintended penalties, that no less than in some circumstances will likely be worse than the issues that the regulation/legislation was supposed to carry in examine. Third, having seen how badly regulators and legislators have dealt with the results of the social media explosion, I’m skeptical that they may even know the place to start out with AI. Whereas it is a pessimistic take, I imagine that it a sensible one, and that simply as with social media, it will likely be as much as us, as customers of AI services and products, to strive to attract traces and separate good from dangerous. We might not succeed, however what alternative do we’ve got, however to strive?

The AI Chip Story

The AI story has explicit resonance with NVIDIA as a result of not like most different corporations, the place it’s largely hand-waving about potential, it has substance in place already and a market that’s its goal. Particularly, NVIDIA has spent a lot of the previous couple of years investing and growing merchandise for a nascent AI market. This lead time has given NVIDIA not simply market management, however revenues and earnings already. A lot of the excited response to NVIDIA’s most up-to-date earnings report got here from the corporate reporting a surge in its information middle revenues, with a lot of the rise coming from AI chips. Whereas the corporate doesn’t explicitly escape how a lot of the info middle revenues are from AI chips, it’s estimated that the entire marketplace for these chips in 2022 was about $15 billion, with NVIDIA holding a dominant market share of about 80%. If these estimates are proper, the majority of the info middle revenues for NVIDIA in 2022, which amounted to $15 billion in all, comes from AI-optimized chips.

The ChatGPT jolt to market expectations has performed out in will increase in anticipated progress of the AI chip market over the following decade, with estimates for the general AI chip market in 2030 starting from $200 billion on the low finish to shut to $300 billion on the excessive finish. Whereas there’s a enormous quantity of uncertainty about this estimate, there are two assertions that may be made about NVIDIA’s presence on this enterprise. The primary is that this would be the progress engine for NVIDIA’s revenues over the following decade, whilst their gaming and different chip income progress ranges off. The second is that NVIDIA has a lead over its competitors, and whereas AMD, Intel and TSMC will all allocate sources to constructing their AI companies, NVIDIA’s dominance is not going to crack simply.

NVIDIA: Valuation and Determination Time

As you take a look at NVIDIA’s progress and success within the final decade, and its current ascent into the rarefied air of “trillion greenback market cap” corporations, there are two impulses that come into play. One is to extrapolate the previous and assume that assume that the corporate will proceed to not simply succeed sooner or later, however accomplish that in a method that beats the market’s expectations for it. The opposite is to argue that the outsized success of the previous has raised buyers expectations a lot that it will likely be troublesome for the corporate to fulfill them. In my story, I’ll draw on each impulses, and attempt to thread the needle on the corporate.

Story and Valuation

The motive force of NVIDIA’s success has been its high-performance GPU playing cards, however it is extremely probably that the companies that purchased these playing cards and drove NVIDIA’s success within the final decade will likely be completely different from the companies that can make it profitable within the subsequent one. For a lot of the final decade, it was gaming and crypto customers that allowed the corporate to set itself other than the competitors, however the dangerous information is that each of those markets are maturing, with decrease anticipated progress sooner or later. The excellent news, for NVIDIA, is that it has two different companies which might be able to step in and contribute to progress. The primary is AI, the place NVIDIA instructions a hefty market share of what’s now a comparatively small market, however one that’s nearly sure to develop ten-fold or better over the last decade. The opposite is within the cars enterprise, the place extra highly effective computing is seen because the ingredient wanted to open up automated driving and different enhancements. NVIDIA is barely a small participant on this house, and whereas it doesn’t benefit from the dominance that it does in AI, a rising market will permit NVIDIA to amass a big market share.

I’ll begin with a well-known assemble (no less than to those that observe my valuations), and break down the inputs that drive worth as a precursor to introducing my NVIDIA story:

Put merely, the worth of an organization is a perform of 4 broad inputs – income progress, as a stand-in for its progress potential, a goal working margin as a proxy for profitability, a reinvestment scalar (I exploit gross sales to invested capital) as a measure of the effectivity with which it delivers progress and a price of capital & failure charge to include threat.

While all of NVIDIA’s completely different companies (AI, Auto, Gaming) share some frequent options when it comes to gross and working margins, and requiring R&D for innovation, the companies are diverging when it comes to income progress potential.

- Income Development: NVIDIA will stay a excessive progress firm for 2 causes. The primary is that regardless of its scaling up on account of progress during the last decade, no less than when it comes to revenues, it has a modest market share of the general semiconductor market, with revenues which might be lower than half of the revenues posted by Intel or TSMC. The second, and extra vital purpose, is that whereas its gaming income progress is beginning to flag, it’s well-positioned in AI and Auto, two markets poised for speedy progress. In my story, I’ll assume that these markets will ship on their progress promise and that NVIDIA will keep a dominant, albeit decrease, market share of the AI chip enterprise, whereas gaining a big share (15%) of the Auto chip enterprise:

Clearly, there may be room for disagreement on each complete market and market share for the AI and Auto companies, and I’ll return to handle the results. I’m nonetheless permitting the gaming and different enterprise revenues to develop at 15% a 12 months, a wholesome quantity that displays different companies (just like the omniverse) contributing to the highest line.

- Profitability: The semiconductor enterprise has a price construction that has comparatively little flex to it, however I’ll assume in my NVIDIA story that the suitable margin to deal with is the R&D adjusted model, and that NVIDIA will bounce again shortly from its 2022 margin setback to ship larger margins than its peer group. Whereas my goal R&D adjusted margin of 40% might look excessive, it’s price remembering that the corporate delivered 42.5% as margin in 2020 and 38.4% as margin in 2021. As famous earlier, NVIDIA’s dependence on TSMC for the manufacturing of the chips it sells implies that any will increase in margins have to come back extra from worth will increase than price efficiencies.

- Funding Effectivity: NVIDIA has invested closely within the final decade, producing solely 65 cents in revenues for each greenback of capital invested (together with the funding in R&D), in 2022. That funding has clearly been productive, as the corporate has been capable of finding progress and generate extra returns. I imagine that given the corporate’s bigger scale, with the payoff from previous investments augmenting revenues, the corporate’s gross sales to invested capital will strategy the worldwide {industry} median, which is $1.15 in revenues for each greenback of capital invested.

- Danger: As we famous within the part on the semiconductor enterprise, this stays, even for its most profitable proponents, a cyclical enterprise, and that cyclicality contributes to retaining the price of capital larger than for the median firm. I estimated NVIDIA’s price of capital based mostly upon its geographic publicity and really low debt ratio to be 13.13%, however selected to make use of the {industry} common for US semiconductor corporations, which was 12.21%, as the price of capital within the preliminary progress interval. Over time, I’ll assume that this price of capital will drift down in the direction of the general market common price of capital of 8.85%.

With this story in place, and the ensuing enter numbers, the worth that I get for NVIDIA is proven beneath:

Primarily based on story, the worth per share that I arrive at for NVIDIA on June 10, 2023, is about $240, nicely beneath the inventory worth of $409 that the inventory traded at on June 10, 2023. (The inventory has risen since then to $434 a share on June 20, 2023.)

Simulation and Breakeven Evaluation

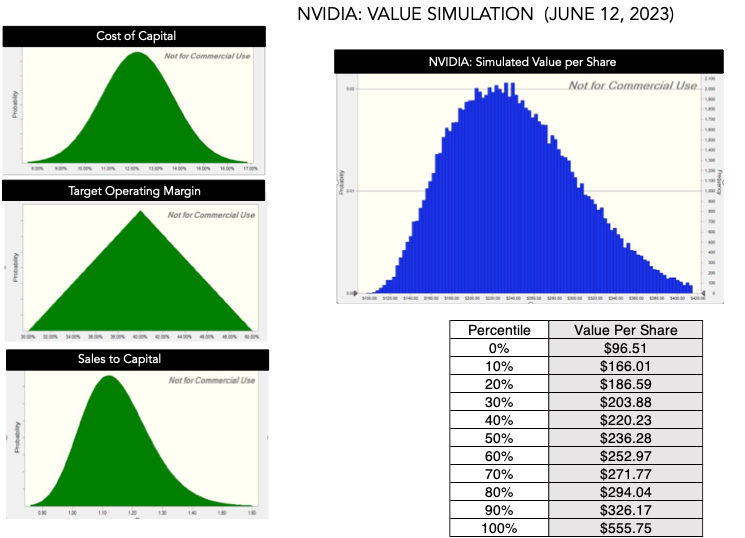

On the threat of stating the plain, I’m making assumptions about market progress and market share that you could be and even ought to take challenge with. Within the pursuits of inspecting how worth varies as a perform of the assumptions, I fell again on an strategy that I discover helps me take care of estimation uncertainty, which is a simulation. I constructed the simulation round the important thing inputs, together with:

-

Revenues: In my base case valuation, incorporating excessive progress within the AI and Auto Chip companies, and giving NVIDIA a dominant share of the primary and a big share of the second resulted in revenues of $267 billion in 2033. Nevertheless, that is constructed on assumptions concerning the future for each markets that may be unsuitable, in both path, and that uncertainty is included into the simulation as distributions for every of the three segments of NVIDIA’s revenues:

As these distributions play out, there are simulations the place NVIDIA’s revenues exceed $600 billion and a few the place it’s lower than $100 billion, in 2033.

- Working Margin: In my base case story, I improve NVIDIA’s R&D adjusted margin to 35% subsequent 12 months, and goal an working margin of 40% in 2027, that it maintains in perpetuity after that. Whereas I present my justifications for these assumptions, it’s fully attainable that I’m being too optimistic, in elevating margins which might be already above industry-average ranges to even larger values, or that I’m being pessimistic, and never factoring in NVIDIA’s larger pricing energy within the AI and Auto companies. I seize that uncertainty in my (triangular) distribution for the goal working margin in 2027 (and past), the place I set the higher finish of the vary at 50%, which might be a big premium over NVIDIA’s personal previous margins, and the decrease finish at 30%, which might put them nearer to their peer group.

- Reinvestment: The enter that drives reinvestment is the gross sales to capital ratio, and whereas I set NVIDIA’s gross sales to capital ratio at 1.15, the semiconductor {industry} common, it’s attainable that the corporate might proceed to reinvest at nearer to its historic common of 0.65 (resulting in extra reinvestment). Alternatively, it’s also conceivable that the corporate’s investments during the last decade, particularly in its AI chips, will put it on a glide path to reinvesting lots much less within the subsequent decade (a gross sales to capital ratio nearer to 1.94, the seventy fifth percentile of the semiconductor enterprise.

- Danger: Ruling out failure threat, and specializing in the price of capital, I middle my estimates on 12.21%, the {industry} common that I used within the base case, however permit for the chance {that a} rising AI enterprise might scale back the cyclicality of revenues, reducing the price of capital in the direction of the market-average of 8.85%) or conversely, improve uncertainty and uncertainty, elevating the price of capital in the direction of 15%, the ninetieth percentile of worldwide corporations):

With these estimates in place, the simulated worth per share is proven beneath:

To the query of whether or not NVIDIA could possibly be price $400 a share or extra, the reply is sure, however the odds, no less than based mostly on my estimates, are low. In actual fact, the present inventory worth is pushing in the direction of the ninety fifth percentile of my worth distribution.

An alternate take a look at what has to occur for NVIDIA’s intrinsic worth to exceed $400, I appeared on the two key variables that decide its worth: revenues in 12 months 10 and working margins:

This desk reinforces the findings within the simulation, insofar because it exhibits that there are believable paths that result in the present worth being a good worth or beneath worth, however these paths require a frightening mixture of extraordinary income progress and super-normal margins. For my part, a goal margin of fifty% is pushing the boundaries of chance, within the semiconductor enterprise, and if NVIDIA finds a option to ship worth that justifies present pricing, it must be via explosive income progress. Put merely, you want one other market or two, with potential just like the AI market, the place NVIDIA can wield a dominant market share to justify its pricing.

Judgment Day

As I famous firstly of this publish, I’ve a egocentric purpose for valuing NVIDIA, which is that I personal it shares and I’m uncovered to its worth actions, and rather more so now than I used to be once I purchased the inventory in 2018, because of its inflated pricing. I’ve additionally been open about the truth that my funding philosophy is constructed round worth, shopping for when worth is lower than worth and by the identical token, promoting when worth is way larger than worth.

NVIDIA as an Funding

I like NVIDIA as an organization, and don’t have anything however reward for Jensen Huang’s management of the corporate. Working in a enterprise the place income progress was changing into scarce (single digit income progress) and segments of the product market are commoditized (reducing margins), NVIDIA discovered a pathway to not simply ship progress, however progress with superior revenue margins and extra returns. Whereas some might argue that NVIDIA was fortunate to catch a progress spurt within the gaming and crypto companies, a more in-depth take a look at its successes means that it was not luck, however foresight, that put the corporate able to succeed. In actual fact, because the AI and Auto companies look poised to develop, NVIDIA’s positioning in each signifies that it is a firm that’s constructed to be opportunistic. My valuation story for NVIDIA displays all of those optimistic options, and assumes that they may proceed into the following decade, however that upbeat narrative nonetheless yields a worth nicely beneath the present worth.

I might be mendacity if I mentioned that promoting certainly one of my greatest winners is simple, particularly since there’s a believable pathway, albeit a low-probability one, that the corporate will be capable to ship strong returns, at present costs. I selected a path that splits the distinction, promoting half of my holdings and cashing in on my earnings, and holding on to the opposite half, extra for the optionality (that the corporate will discover different new markets to enter within the subsequent decade). The worth purists can argue, with justification, that I’m appearing inconsistently, given my worth philosophy, however I’m pragmatist, not a purist, and this works for me. It does open up an attention-grabbing query of whether or not it’s best to proceed to carry a inventory in your portfolio that you wouldn’t purchase at at present’s inventory costs, and it’s one which I’ll return to in a future publish.

NVIDIA as a Commerce

I’ve written many posts concerning the divide between investing and buying and selling, arguing that the 2 are philosophically completely different. In investing, you assess the worth of a inventory, examine that worth to the value, act on that distinction (shopping for when worth is lower than worth and promoting when it’s better) and hope to earn cash because the hole between worth and worth closes. In buying and selling, you purchase at a low worth, hoping to promote at the next worth, however you’re agnostic about what causes the value to maneuver and whether or not that motion is rational or not.

Bringing this distinction to play in NVIDIA, you’ll be able to see why, it doesn’t matter what you concentrate on NVIDIA’s worth, you might proceed to commerce it. Thus, even for those who imagine that NVIDIA’s worth is nicely beneath its worth, you might purchase NVIDIA on the expectation that the inventory will proceed to rise, borne upwards by momentum or incremental info. Given the energy of momentum as a market-driver, you might very nicely generate excessive returns over the following weeks, months and even years, and you shouldn’t let “worth scolds” get in the way in which of your enjoyment of your winnings. My solely pushback can be towards those that argue that momentum can carry a inventory ahead perpetually, since it’s the reward that each provides and takes away. The energy of momentum within the rise in NVIDIA’s inventory worth will likely be performed out within the the other way, when (not if) momentum shifts, and if you’re buying and selling NVIDIA, you ought to be engaged on indicators that offer you early warning of these shifts, not worrying about worth.

The Backside Line

As we hear the relentless pitches for AI, and the way it will change our reside and have an effect on our investments, there are classes, to attract on, from the opposite large adjustments that we’ve got seen over our lifetime. The primary is that even for those who purchase into the argument that AI will change the ways in which we work and play, it doesn’t essentially observe that investing in AI-related corporations will yield returns. In different phrases, you will get the macro story proper, however you’ll want to additionally think about how that story performs out throughout corporations to have the ability to generate returns. The second, is that refusing to make estimates or judgments about how AI will have an effect on the basics (money flows, progress and threat) in a enterprise, simply since you face vital uncertainty, is not going to make that uncertainty go away. As an alternative, it is going to create a vacuum that will likely be crammed by arbitrary AI premiums and make us extra uncovered to scams and wannabes. The third is that, as a society, it’s unclear whether or not including AI to the combination will make us higher or worse off, since each large technological change appears to carry with it unintended penalties. To finish, I used to be contemplating asking ChatGPT to jot down this publish for me, utilizing my very own language and historical past, and I’m open to the chance that it might do a greater job than I’ve. Keep tuned!

YouTube

Spreadsheets