[ad_1]

As I reveal my ignorance about TikTok developments, social media celebrities and Gen Z slang, my youngsters are fast to level out my age, and I settle for that actuality, for essentially the most half. I perceive that I’m too outdated to train with out stretching first or eat a heaping plate of cheese fries and never endure heartburn, however that doesn’t cease me from making an attempt often. For the final decade or so, I’ve argued that companies, like human beings, age, and battle with ageing, and that a lot of the dysfunction we observe of their choice making stems from refusing to behave their age. Actually, the enterprise life cycle has turn out to be an integral a part of the company finance, valuation and investing lessons that I educate, and in lots of the posts that I’ve written on this weblog. In 2022, I made a decision that I had hit crucial mass, by way of company life cycle content material, and that the fabric may very well be organized as a guide. Whereas the writing for the guide was largely finished by November 2022, publishing does have a protracted lead time, and the guide, revealed by Penguin Random Home, can be accessible on August 20, 2024, at a guide store close to you. If you’re involved that you’re going to be hit with a gross sales pitch for that guide, removed from it! Quite than attempt to half you out of your cash, I assumed I’d give a compressed model of the guide on this publish, and for many of you, that can suffice.

Setting the Stage

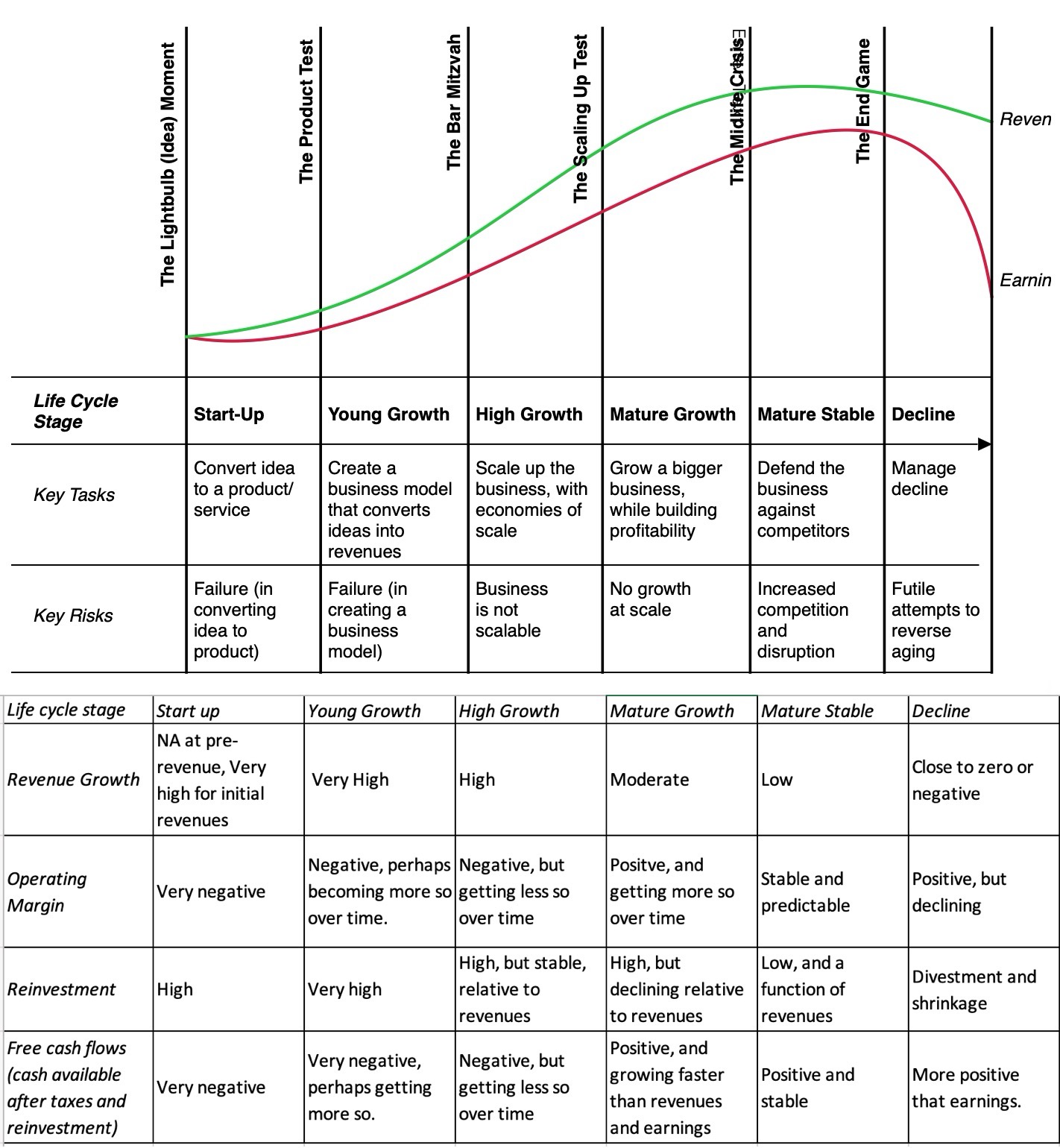

My model of the company life cycle is constructed round six levels with the primary stage being an thought enterprise (a start-up) and the final one representing decline and demise.

As you possibly can see, the important thing duties shift as enterprise age, from constructing enterprise fashions within the excessive progress section to scaling up the enterprise in excessive progress to defending towards competitors within the mature section to managing decline int he final section. Not surprisingly, the working metrics change as firms age, with excessive income progress accompanied by massive losses (from work-in-progress enterprise fashions) and enormous reinvestment wants (to supply future progress) in early-stage firms to giant earnings and free money flows within the mature section to stresses on progress and margins in decline. Consequently, by way of money flows, younger firms burn by way of money, with the burn rising with potential, money buildup is frequent as firms mature adopted by money return, as the conclusion kicks in that an organization’s excessive progress days are prior to now.

As firms transfer by way of the life cycle, they’ll hit transition factors in operations and in capital elevating that should be navigated, with excessive failure charges at every transition. Thus, most thought companies by no means make it to the product section, many product firms are unable to scale up, and fairly a number of scaled up corporations are unable to defend their companies from opponents. Briefly, the company life cycle has far increased mortality charges as companies age than the human life cycle, making it crucial, in case you are a enterprise individual, that you simply discover the unusual pathways to outlive and develop.

Measures and Determinants

In case you purchase into the notion of a company life cycle, it stands to purpose that you prefer to a method to decide the place an organization stands within the life cycle. There are three selections, every with pluses and minuses.

- The primary is to deal with company age, the place you estimate how outdated an organization is, relative its founding date; it’s straightforward to acquire, however firms age at completely different charges (as nicely will argue within the following part), making it a blunt weapon.

- The second is to have a look at the business group or sector that an organization is in, after which comply with up by classifying that business group or sector into excessive or low progress; for the final 4 many years, in US fairness markets, tech has been seen as progress and utilities as mature. Right here once more, the issue is that prime progress business teams start to mature, simply as firms do, and this has been true for some segments of the tech sector.

- The third is to deal with the working metrics of the agency, with corporations that ship excessive income progress, with low/adverse earnings and adverse free money flows being handled as younger corporations. It’s extra data-intensive, since making a judgment on what contains excessive (income progress or margins) requires estimating these metrics throughout all corporations.

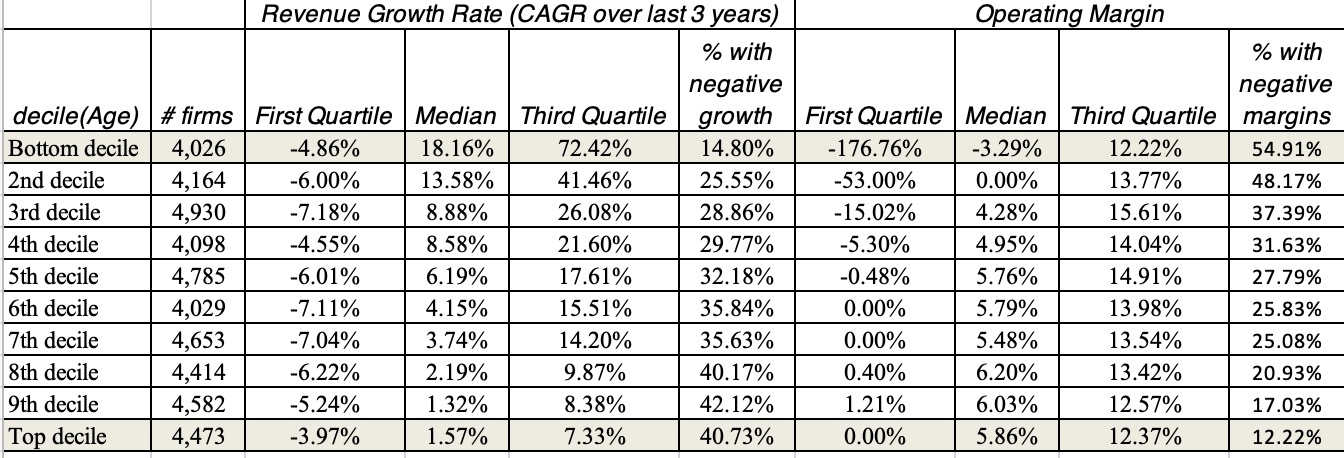

Whereas I delve into the main points of all three measures, company age works surprisingly nicely as a proxy for the place an organization falls within the life cycle, as might be seen on this desk of all publicly traded firms listed globally, damaged down by company age into ten deciles:

As you possibly can see, the youngest firms have a lot increased income progress and extra adverse working margins than older firms.

In the end, the life cycles for firms can fluctuate on three dimensions – size (how lengthy a enterprise lasts), top (how a lot it could possibly scale up earlier than it plateaus) and slope (how rapidly it could possibly scale up). Even a cursory look on the firms that encompass it’s best to let you know that there are large variations throughout firms, on these dimensions. To see why, contemplate the elements that decide these life cycle dimensions:

Firms in capital-light companies, the place prospects are keen to change from the established order, can scale up a lot sooner than firms in capital-intensive companies, the place model names and buyer inertia could make breakthroughs tougher. It’s price noting, although, that the forces that enable a enterprise to scale up rapidly usually restrict how lengthy it could possibly keep on the prime and trigger decline to be faster, a commerce off that was ignored over the past decade, the place scaling up was given primacy.

The drivers of the company life cycle also can clarify why the standard twenty-first century firm faces a compressed life cycle, relative to its twentieth century counterpart. Within the manufacturing-centered twentieth century, it took many years for firms like GE and Ford to scale up, however in addition they stayed on the prime for lengthy durations, earlier than declining over many years. The tech-centered economic system that we reside in is dominated by firms that may scale up rapidly, however they’ve temporary durations on the prime and scale down simply as quick. Yahoo! and BlackBerry soared from begin ups to being price tens of billions of {dollars} in a blink of an eye fixed, had temporary reigns on the prime and melted right down to nothing virtually as rapidly.

Tech firms age in canine years, and the results for a way we handle, worth and put money into them are profound. Actually, I’d argue that the teachings that we educate in enterprise college and the processes that we use in evaluation want adaptation for compressed life cycle firms, and whereas I haven’t got all of the solutions, the dialogue about altering practices is a wholesome one.

Company Finance throughout the Life Cycle

Company finance, as a self-discipline, lays out the primary rules that govern how one can run a enterprise, and with a deal with maximizing worth, all selections {that a} enterprise makes might be categorized into investing (deciding what belongings/tasks to put money into), financing (selecting a mixture of debt and fairness, in addition to debt sort) and dividend selections (figuring out how a lot, if any, money to return to house owners, and in what type).

Whereas the primary rules of company finance don’t change as an organization ages, the main focus and estimation processes will shift, as proven within the image under:

With younger firms, the place the majority of the worth lies in future progress, and earnings and money flows are sometimes adverse, it’s the funding choice that dominates; these firms can’t afford to borrow or pay dividends. With extra mature firms, as funding alternatives turn out to be scarcer, at the very least relative to accessible capital, the main focus not surprisingly shifts to financing combine, with a decrease hurdle charge being the repay. With declining companies, going through shrinking revenues and margins, it’s money return or dividend coverage that strikes into the entrance seat.

Valuation throughout the Life Cycle

I’m fascinated by valuation, and the hyperlink between the worth of a enterprise and its fundamentals – money flows, progress and danger. I’m additionally a realist and acknowledge that I reside in a world, the place pricing dominates, with what you pay for an organization or asset being decided by what others are paying for comparable firms and belongings:

All firms might be each valued and priced, however the absence of historical past and excessive uncertainty concerning the future that characterizes younger firms makes it extra possible that pricing will dominate valuation extra decisively than it does with extra mature corporations.

All companies, irrespective of the place they stand within the life cycle, might be valued, however there are key variations that may be off placing to some. A nicely finished valuation is a bridge between tales and numbers, with the interaction figuring out how defensible the valuation is, however the stability between tales and numbers will shift, as you progress by way of the life cycle:

With younger firms, absent historic information on progress and profitability, it’s your story for the corporate that can drive your numbers and worth. As firms age, the numbers will turn out to be extra essential, because the tales you inform can be constrained by what you might have been in a position to ship in progress and margins. In case your power as an analyst or appraiser is in bounded story telling, you may be higher served valuing younger firms, whereas in case you are a number-cruncher (comfy with accounting ratios and elaborate spreadsheet fashions), you will see that valuing mature firms to be your pure habitat.

The draw of pricing is robust even for many who declare to be believers in worth, and pricing in its easiest type requires a standardized value (a a number of like value earnings or enterprise worth to EBITDA) and a peer group. Whereas the pricing course of is similar for all firms, the pricing metrics you utilize and the peer teams that you simply examine them to will shift as firms age:

For pre-revenue and really younger firms, the pricing metrics will standardize the value paid (by enterprise capitalists and different traders) to the variety of customers or subscribers that an organization has or to the whole market that its product is aimed toward. As enterprise fashions develop, and revenues come into play, you’re more likely to see a shift to income multiples, albeit usually to estimated revenues in a future 12 months (ahead numbers). Within the mature section, you will notice earnings multiples turn out to be extra broadly used, with fairness variations (like PE) in peer teams the place leverage is analogous throughout firms, and enterprise worth variations (EV to EBITDA) in peer teams, the place leverage is completely different throughout firms. In decline, multiples of guide worth will turn out to be extra frequent, with guide worth serving as a (poor) proxy for liquidation or break up worth. Briefly, if you wish to be open to investing in firms throughout the life cycle, it behooves you to turn out to be comfy with completely different pricing ratios, since nobody pricing a number of will work on all corporations.

Investing throughout the Life Cycle

In my class (and guide) on funding philosophies, I begin by noting that each funding philosophy is rooted in a perception about markets making (and correcting) errors, and that there isn’t a one greatest philosophy for all traders. I take advantage of the funding course of, beginning with asset allocation, transferring to inventory/asset choice and ending with execution to indicate the vary of views that traders deliver to the sport:

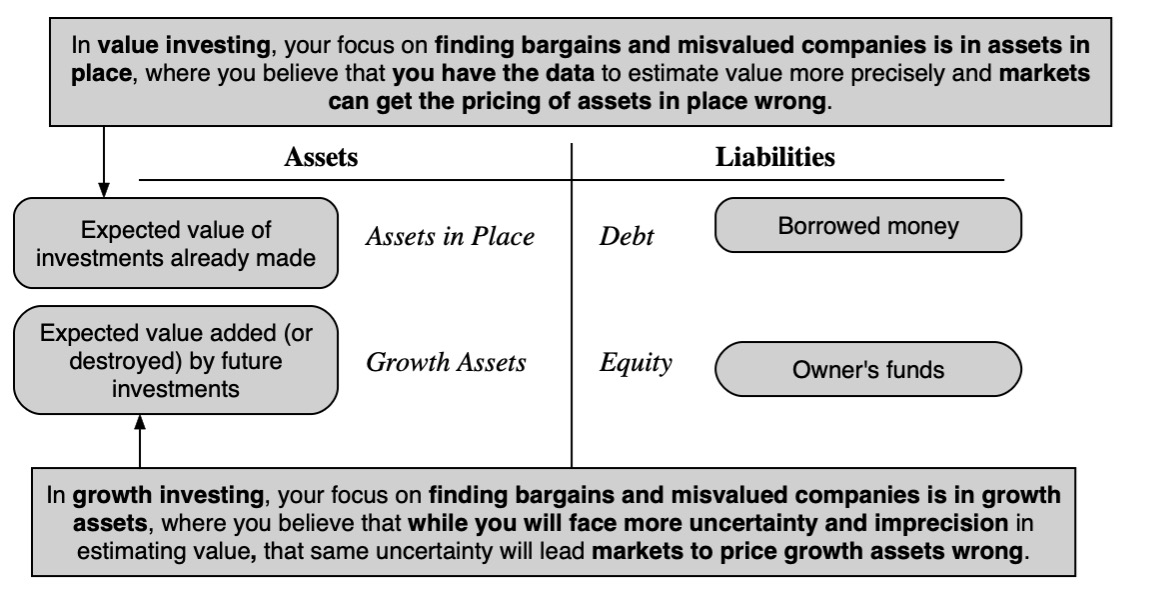

Market timing, whether or not it’s primarily based on charts/technical indicators or fundamentals, is primarily centered on the asset allocation section of investing, with cheaper (primarily based upon your market timing measures) asset lessons being over weighted and dearer asset lessons being below weighted. Throughout the inventory choice section, there are an entire host of funding philosophies, usually holding contradictory views of market conduct. Amongst inventory merchants, for example, there are those that imagine that markets be taught slowly (and go together with momentum) and people who imagine that markets over react (and guess on reversals). On the investing aspect, you might have the traditional divide between worth and progress traders, each claiming the excessive floor. I view the variations between these two teams by way of the prism of a monetary stability sheet:

Worth traders imagine that the very best funding bargains are in mature firms, the place belongings in place (investments already made) are being underpriced by the market, whereas progress traders construct their funding theses round the concept it’s progress belongings the place markets make errors. Lastly, there are market gamers who attempt to earn money from market frictions, by locking in market mispricing (with pure or close to arbitrage).

Drawing on the sooner dialogue of worth versus value, you possibly can classify market gamers into traders (who worth firms, and attempt to purchase them at a cheaper price, whereas hoping that the hole closes) and merchants (who make them cash on the pricing sport, shopping for at a low value and promoting at the next one). Whereas traders and merchants are a part of the market in each firm, you’re more likely to see the stability between the 2 teams shift as firms transfer by way of the life cycle:

Early within the life cycle, it’s plain that merchants dominate, and for traders in these firms, even when they’re proper of their worth assessments, successful would require for much longer time horizons and stronger stomachs. As firms mature, you’re more likely to see extra traders turn out to be a part of the sport, with cut price hunters getting into when the inventory drops an excessive amount of and quick sellers extra keen to counter when it goes up an excessive amount of. In decline, as authorized and restructuring challenges mount, and an organization can have a number of securities (convertibles, bonds, warrants) buying and selling on it, hedge funds and activists turn out to be greater gamers.

In sum, the funding philosophy you select can lead you to over put money into firms in some phases of the life cycle, and whereas that by itself will not be an issue, denying that this skew exists can turn out to be one. Thus, deep worth investing, the place you purchase shares that commerce at low multiples of earnings and guide worth, will lead to bigger parts of the portfolio being invested in mature and declining firms. That portfolio will benefit from stability, however anticipating it to include ten-baggers and hundred-baggers is a attain. In distinction, a enterprise capital portfolio, invested virtually totally in very younger firms, could have a lot of wipeouts, however it could possibly nonetheless outperform, if it has a number of giant winners. Recommendation on concentrating your portfolio and having a margin of security, each worth investing nostrums, may fit with the previous however not with the latter.

Managing throughout the Life Cycle

Administration specialists who educate at enterprise faculties and populate the premier consulting corporations have a lot to achieve by propagating the parable that there’s a prototype for an excellent CEO. In any case, it offers them a purpose to cost nose-bleed costs for an MBA (to be imbued with these qualities) or for consulting recommendation, with the identical finish sport. The reality is that there isn’t a one-size-fits-all for an excellent CEO, because the qualities that you’re in search of in prime administration will shift as firms age:

Early within the life cycle, you need a visionary on the prime, since it’s important to get traders, workers and potential prospects to purchase into that imaginative and prescient. To show the imaginative and prescient into services and products, although, you want a pragmatist, keen to just accept compromises. As the main focus shifts to enterprise fashions, it’s the business-building expertise that make for an excellent CEO, permitting for scaling up and success. As a scaled-up enterprise, the ability units change once more, with opportunism turning into the important thing high quality, permitting the corporate to seek out new markets to develop in. In maturity, the place taking part in protection turns into central, you need a prime supervisor who can guard an organization’s aggressive benefits fiercely. Lastly, in decline, you need CEOs, unencumbered by ego or the will to construct empires, who’re keen to preside over a shrinking enterprise, with divestitures and money returns excessive on the to-do listing.

There are only a few individuals who have all of those expertise, and it ought to come as no shock that there could be a mismatch between an organization and its CEO, both as a result of they (CEO and firm) age at completely different charges or due to hiring errors. These mismatches might be catastrophic, if a headstrong CEO pushes forward with actions which are unsuited to the corporate she or he is in cost off, however they are often benign, if the mismatched CEO can discover a associate who can fill in for weaknesses:

Whereas the chances of mismatches have at all times been a part of enterprise, the compression of company life cycles has made them each more likely, in addition to extra damaging. In any case, time took care of administration transitions for long-lived twentieth century corporations, however with corporations that may scale as much as turn out to be market cap giants in a decade, earlier than cutting down and disappearing within the subsequent one, you possibly can very nicely see a founder/CEO go from being a hero in a single section to a zero within the subsequent one. As we now have allowed lots of the most profitable corporations which have gone public on this century to skew the company finance sport, with shares with completely different voting rights, we could also be dropping our energy to alter administration at these corporations the place the necessity for change is biggest.

Growing older gracefully?

The healthiest response to ageing is acceptance, the place a enterprise accepts the place it’s within the life cycle, and behaves accordingly. Thus, a younger agency that derives a lot of its worth from future progress mustn’t put that in danger by borrowing cash or by shopping for again inventory, simply as a mature agency, the place worth comes from its current belongings and aggressive benefits, mustn’t danger that worth by buying firms in new and unfamiliar companies, in an try to return to its progress days. Acceptance is most tough for declining corporations, because the administration and traders should make peace with downsizing the agency. For these corporations, it’s price emphasizing that acceptance doesn’t indicate passivity, a distorted and defeatist view of karma, the place you do nothing within the face of decline, however requires actions that enable the agency to navigate the method with the least ache and most worth to its stakeholders.

It ought to come as no shock that many corporations, particularly in decline, select denial, the place managers and traders provide you with excuses for poor efficiency and lay blame on outdoors elements. On this path, declining corporations will proceed to behave the way in which they did after they have been mature and even progress firms, with giant prices to everybody concerned. When the promised turnaround doesn’t ensue, desperation turns into the choice path, with managers playing giant sums of different folks’s cash on lengthy pictures, with predictable outcomes.

The siren track that pulls declining corporations to make these makes an attempt to recreate themselves, is the hope of a rebirth, and an ecosystem of bankers and consultants affords them magic potions (taking the type of proprietary acronyms that both restate the plain or are constructed on foundations of made-up information) that can make them younger once more. They’re aided and abetted by case research of firms that discovered pathways to reincarnation (IBM in 1992, Apple in 2000 and Microsoft in 2013), with the added bonus that their CEOs have been elevated to legendary standing. Whereas it’s plain that firms do generally reincarnate, it’s price recognizing that they continue to be the exception relatively than the rule, and whereas their prime administration deserves plaudits, luck performed a key function as nicely.

I’m a skeptic on sustainability, at the very least as utilized to firms, since its makes company survival the tip sport, generally with substantial prices for a lot of stakeholders, in addition to for society. Just like the Egyptian Pharaohs who sought immortality by wrapping their our bodies in bandages and being buried with their favourite possessions, firms that search to reside endlessly will turn out to be mummies (and generally zombies), sucking up assets that may very well be higher used elsewhere.

In conclusion

It’s the dream, in each self-discipline, to provide you with a idea or assemble that explains all the things in that disciple. In contrast to the bodily sciences, the place that search is constrained by the legal guidelines of nature, the social sciences mirror extra trial and error, with the unpredictability of human nature being the wild card. In finance, a self-discipline that began as an offshoot of economics within the Nineteen Fifties, that search started with theory-based fashions, with portfolio idea and the CAPM, veered into data-based constructs (proxy fashions, issue evaluation), and behavioral finance, with its marriage of finance and psychology. I’m grateful for these contributions, however the company life cycle has supplied me a low-tech, however surprisingly large reaching, assemble to clarify a lot of what I see in enterprise and funding conduct.

If you end up within the subject, you possibly can attempt the guide, and within the pursuits of creating it accessible to a various reader base, I’ve tried to make it each modular and self-standing. Thus, in case you are concerned with how operating a enterprise adjustments, because it ages, you possibly can deal with the 4 chapters that have a look at company finance implications, with the lead-in chapter offering you adequate of a company finance basis (even when you’ve got by no means taken a company finance class) to have the ability to perceive the investing, financing and dividend results. If you’re an appraiser or analyst, concerned with valuing firms throughout the life cycle, it’s the 5 chapters on valuation that will draw your curiosity, once more with a lead-in chapter containing an introduction to valuation and pricing. As an investor, it doesn’t matter what your funding philosophy, it’s the 4 chapters on investing throughout the life cycle that will enchantment to you essentially the most. Whereas I’m positive that you’ll have no bother discovering the guide, I’ve an inventory of guide retailers listed under that you should use, should you select, and the webpage supporting the guide might be discovered right here.

If you’re budget-constrained or simply do not like studying (and there’s no disgrace in that), I’ve additionally created an internet class, with twenty classes of 25-35 minutes apiece, that delivers the fabric from the guide. It consists of workout routines that you should use to verify your understanding, and the hyperlink to the category is right here.

YouTube Video

Guide and Class Webpages

- Guide webpage: https://pages.stern.nyu.edu/~adamodar//New_Home_Page/CLC.htm

- Class webpage: https://pages.stern.nyu.edu/~adamodar//New_Home_Page/webcastCLC.htm

- YouTube Playlist for sophistication: https://www.youtube.com/playlist?listing=PLUkh9m2BorqlpbJBd26UEawPHk0k9y04_

Hyperlinks to booksellers

- Amazon: https://www.amazon.com/Company-Lifecycle-Funding-Administration-Implications/dp/0593545060

- Barnes & Noble: https://www.barnesandnoble.com/w/the-corporate-life-cycle-aswath-damodaran/1143170651?ean=9780593545065

- Bookshop.org: https://bookshop.org/p/books/the-corporate-lifecycle-business-investment-and-management-implications-aswath-damodaran/19850366?ean=9780593545065

- Apple: https://books.apple.com/us/audiobook/the-corporate-life-cycle-business-investment/id1680865376

(There may be an Indian version that can be launched in September, which ought to be accessible in bookstores there.)

[ad_2]