[ad_1]

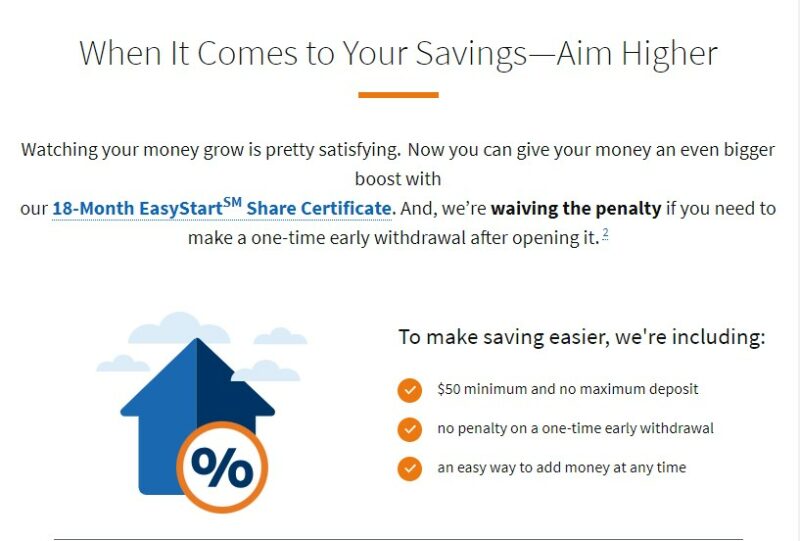

Reader Mike despatched me an intriguing certificates of deposit provide from Navy Federal Credit score Union – their Restricted-Time Provide: 18-Month EasyStart Share Certificates. It is a no-penalty add-on CD with an 18-month time period, coupling two options I’ve by no means seen collectively (but).

I’ve no relationship with Navy Federal Credit score Union, so I am unable to communicate to the expertise of utilizing their CDs, however Mike did and mentioned that he beforehand had an add-on CD that labored properly:

However, I’ve one from an analogous provide they made final 12 months. It was a 15-month add-on CD (not a no penalty CD), APY was 5.0% and I’ve made a small deposit each month since I opened it.

Here is why I discover it attention-grabbing:

- It is a no-penalty CD – 7 days after opening, you can also make one full or partial withdrawal from the CD with out paying a penalty.

- It is an add-on CD – you’ll be able to add cash to the CD at any time throughout the time period.

The present yield on the CD is 4.70% APY, which is lower than the highest no penalty CD charges and excessive yield financial savings account charges. The speed is a bit decrease for that flexibility but it surely’s nonetheless higher than what you’d get for a conventional CD at your native brick and mortar financial institution.

Banking merchandise have gotten extra versatile

It appears there is a development in the direction of banking merchandise changing into extra versatile.

Earlier than smartphones and on-line banks, you had a checking account, financial savings account, and certificates of deposits. You could possibly solely transact six occasions on a financial savings account or face penalties. Your checking account was meant for transactions and paid you no curiosity. All the things else was “financial savings,” and even then, the curiosity was horrible. CDs have been strict – you possibly can solely deposit cash as soon as and have been penalized closely for withdrawing your cash earlier than the CD matured.

These days, it looks like it is all getting blended collectively, particularly in case you are working with a web-based financial institution. Checking accounts pay curiosity, although financial savings and CDs pay extra. And they’ve even suspended the 6 ACH rule, so you’ll be able to have as many transfers as you need between financial savings and checking.

Lastly, you’ve all types of CDs – no-penalty, add-on, no-penalty add-on, bump-up, and so forth. And with on-line banking, it is change into even simpler to open up a CD. You do not have to go to a department and speak to a teller or banker, you are able to do it fully on-line or by the app.

This newest provide from Navy Federal Credit score Union exemplifies this development in the direction of flexibility. Now you may get a CD you could withdraw from with out penalty and add to it everytime you need.

Is that this the long run?

Personally, it is most likely a response to how straightforward it’s to open a CD.

The CD has a minimal of $50 so for those who actually wished flexibility, you’ll be able to open a number of small CDs after which Navy Federal has to cope with all of the paperwork (most likely computerized anyway however nonetheless). The add-on characteristic is much less wonderful whenever you understand you’ll be able to simply hold opening extra CDs. On this case, you realize what the speed is and in a falling charge surroundings, that may be a profit.

I believe that most of these CDs are just like bump-up CDs, the place in a rising charge surroundings you’ll be able to bump up the rate of interest of a CD to the prevailing charge. They exist partly as a result of prospects have such low friction in altering merchandise.

Up to now, you needed to go to a department and transact in particular person. It is means quicker now.

Am I actually going to waste an hour going to the financial institution to get 0.10% APY increased? No means.

Will I spend 5 minutes on my telephone whereas I am ready round? Positive.

I am wanting to see if this development turns into the norm.

[ad_2]